.jpg&q=95&w=400)

Key Points

- May is Home Remodeling Month

- The home improvement industry is flourishing

- Not all home renovations deliver the same ROI

- Top 10 home renovation projects with max ROI (according to Zonda Media’s 2023 Cost vs. Value Report)

- Greenway’s Home Renovation Loans

Happy May and Happy Home Remodeling Month! We’re excited to share with you this some of this year's top 10 home improvement projects that have the highest ROI.

If you’re planning on selling your home in 2023 or if you’re simply looking to do some home renovation projects you’ve come to the right place. With the red hot real estate market, home prices rising, and competition among home buyers fierce, any upgrades you make to your home could go a long way in increasing your home’s value while making it even more appealing to buyers if you’re planning on selling.

The Home Improvement Industry

It’s no surprise that the home improvement industry is flourishing. During the pandemic and even now, Americans have truly learned the importance of “home”. In fact, the total amount spent on home renovations and upgrades soared by nearly 27% between 2020 and 2022, according to TodaysHomeowner.com. We think that says a lot!

Statistics from the Joint Center for Housing Studies of Harvard University (JCHS), show that homeowners spent $337 billion on home improvements and repairs in 2020, $368 billion in 2021, and an estimated $427 billion in 2022. Home improvements are expected to grow even more in 2023 and they will continue to grow as high mortgage rates will entice homeowners to renovate their homes instead of selling.

What Exactly is ROI?

ROI stands for “return on investment" and it is used to measure how much of an investment you could get back when you sell your home. It’s important to note that different home improvements yield different ROIs.

According to DesignerPremier.com, in 2023, a home improvement project’s average ROI is 56%. What does that mean? If a homeowner sells their home, they’ll receive $56 back for every $100 spent on home improvements.

Exterior projects have the highest ROI, some over 100%. Creating outdoor spaces was (and still is) a top priority for homeowners during Covid since many of us couldn’t leave our homes or go on that planned vacation.

Before You Start Your Home Remodeling Project

Before starting any project, you'll want to take into consideration these 3 things.

-

First, the real estate market. If you want to increase your resale value, speak with your local real estate agent. They’ll be able to assess your home to let you know if the improvements you want to make will add value.

-

Second, your budget. Determine how much you can afford before starting any home renovation project.

- Last, decide if you’ll attempt the home improvement project yourself (DIY) or if you'll hire a professional to do the job. It’s important to take all of this into consideration before moving forward especially because hiring a professional can cost a bit more!

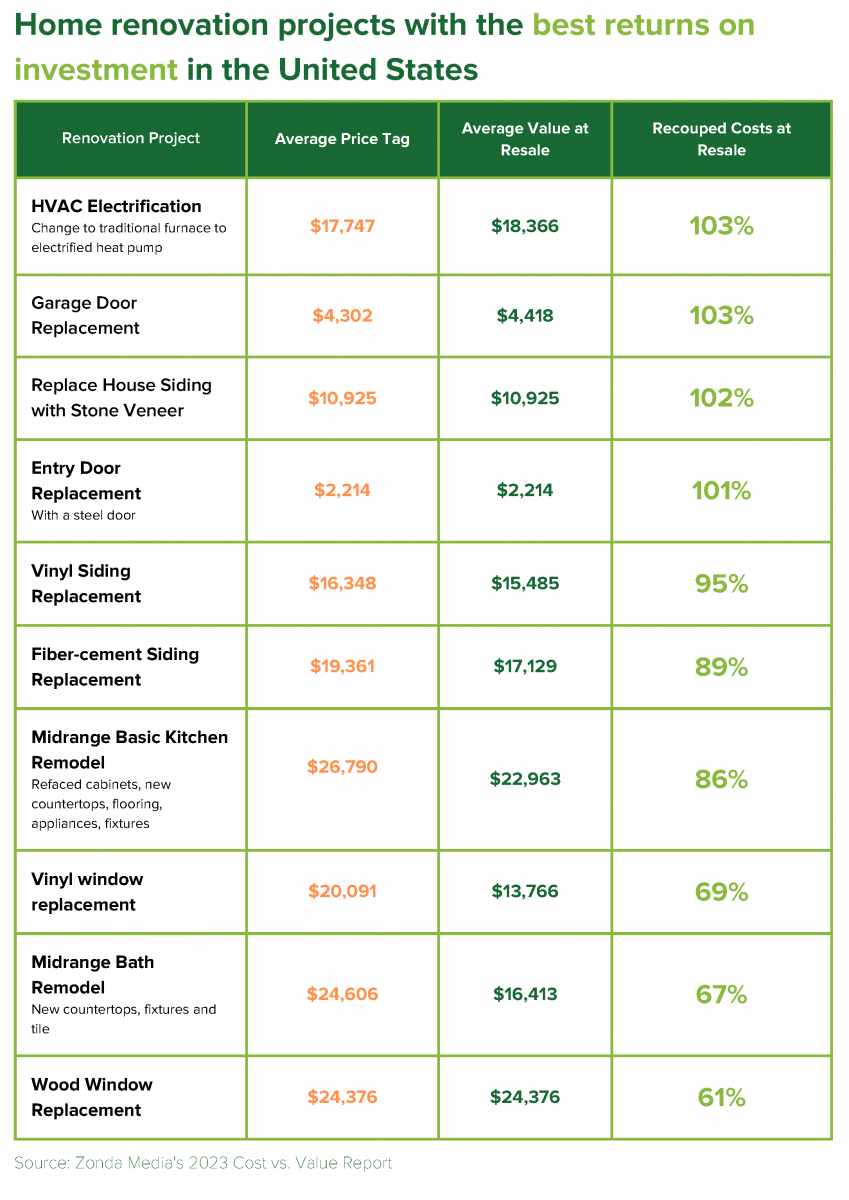

Are you ready to take your home to the next level? Here’s a list of the top 10 home renovation projects that yield that best ROI in the United States.

Source: Zonda Media's 2023 Cost vs. Value report

As you can see, only a few projects could deliver a 100% return on investment like converting a heating, ventilation, and AC system to electric.

Kitchens are a huge selling point and can be one of the most expensive rooms to remodel fully, but a minor kitchen renovation can get you an 86% ROI. If a kitchen remodel is on your list, think about updating the cabinets and countertops, giving your kitchen a fresh coat of paint, or updating the backsplash. Small enhancements like these will provide a high return. Don’t forget the bathroom! A minor bathroom remodel (new countertops, fixtures, and tile) yields a 67% ROI. Major remodels aren't always necessary.

Another easy home renovation project to tackle is the garage door as this is something potential home buyers notice first. Your ROI here is 103%. Need a new front door? A new entry door is another crucial aspect of the home’s perceived value. Investing in a new front (steel) door has an average ROI of 101%.

Replacing old draft windows with new ones can give you a ROI of 69%. A quality vinyl window will also save you money on energy bills because the insulation in the frame of the window itself is energy efficient. Additionally, vinyl windows require no maintenance because they never need painting or scraping. It's clear, vinyl windows give you a great bang for your buck!

Did we mention we offer Energy Efficient Mortgages? Click here to learn more.

Bottom Line:

With home prices on the rise and a tight supply of homes on the market, more people are choosing to fix up their current home rather than looking for a new house.

If a home renovation is on your road map this year, you may want to consider a Home Renovation Loan from Greenway Mortgage. Whether your home improvement projects are large or small, a renovation loan can help you get the job done and it’ll improve the overall value of your home as well.

Although you may be able to pay for home improvements with a personal loan or other types of financing, these methods have higher interest rates and monthly payments.

Instead, you can combine the purchase price plus the renovation costs into one mortgage payment or refinance your existing mortgage plus construction costs into a new mortgage. Our renovation programs make it easy for you to improve your property by including the extra financing in a purchase or refinance loan.

Our Renovation Loans Include:

- FHA 203 K Program

- Streamlined 203K

- Standard 203K

- HomeStyle

If you’re interested in learning more about how a Renovation Loan can help you, contact us today or visit our website here.

.png)

Are you wondering how much you may be able to afford for your home purchase? It pays to know before you look for a home so you can focus on properties that are truly in your comfort range.

How Does Pre-Qualification Work?

Pre-qualifying for a home loan is the easiest way. Here’s how it works. To determine how much you may be able to borrow, we’ll ask questions regarding the source and consistency of your income and savings. We’ll also inquire about any existing debts you may have for cars, credit cards, education, or other types of loans. This is important because not all income can be used to qualify, and any ongoing monthly debts you have will reduce the amount considered available for your housing expenses.

Once we’ve completed the Q&A, we can calculate how much you may be qualified to borrow and how that translates into a comfortable home price. This will be based on:

- Current Rates

- Loan Type

- Down Payment

- Average Tax

- Insurance Rates

Some mortgage payments may also include mortgage insurance or fees for a homeowners association, condominium, or co-op. We’ll take this into consideration too. Keep in mind that qualification factors can vary for different loan programs, and final approval can depend on other factors, such as credit scores and funds to close.

Work With An Experienced Mortgage Lender

With our experience we can help you discover the best programs and strategies to reach your dream home goals. That’s why it’s always worth your while to talk to us before you shop for a home. Want to learn how much home is within your grasp today? Reach out when you’re ready, and we’ll be happy to help.

Helpful Resources

- Loan Programs

- Pre-Approval Request

- Homebuyer Guide

- First-Time Homebuyer Resources

- Meet The Greenway Team

.png)

Did you know that investment funds may be hiding in your mortgage? It's true! You may have more to invest than you think.

A mortgage is the single largest liability most people ever assume. Do your realize its proper management is as important as for any investment?

30-Year vs 15-Year Loan

Which is best the best option? A 30-year or a 15-year loan? Many homeowners want to pay their home loan off as soon as possible, but the value of putting their money into long-term savings and investments often trumps a rapid amortization of principal.

Why pay down the balance on a home loan, only to borrow again later to pay for the kids' college?

The differential savings of a 30-year loan vs. a 15-year option can be put in a 529 plan instead. The result is tax-advantaged growth over time and no uncertainty of borrowing at a potentially high rate later.

Have questions or want to learn more. Reach out! The Greenway Team would love to help and answer any questions you may have.

New Year, New Home? Understanding how to make an offer on your dream home will be key to getting the best deal possible. And we’ve got the “how-to” guide just for you; and there’s only easy steps to follow. We’ll outline them below.

#1: Get Pre-Approved

First and foremost, step number one should always be getting preapproved. Getting pre-approved is the real deal, especially if you’re serious about purchasing a home.

A pre-approval letter is a statement from the lender that you qualify for a specific mortgage amount based on an underwriter's review of all of your financing information ( credit report, pay stubs, bank statement, assets, salary, etc).

Having that pre-approval letter puts you at an advantage when dealing with a potential seller, as he or she will know you're ONE step closer to getting an actual mortgage. In addition, it will help you beat out the competition, negotiate with power, and let you know how much you can afford so you can start saving for a down payment!

What do you need to get preapproved? Here’s a quick overview of some items you’ll need to gather:

- Pay stubs – last 30 days

- W2s – last 2 years

- Federal tax returns – last 2 years, all pages and schedules

- Bank statements – Last 2 months, all pages

- Realtor and attorney contact info

- Copy of photo ID – must be legible

#2 Find Your Dream Home

Buying a home will be one of the biggest financial purchases of your life. Having a Real Estate Agent by your side will be extremely beneficial. Not only will they be able to help you find the perfect home, but they’ll be able to negotiate the contract and terms as well as make a competitive offer that is within your budget.

Need help finding a realtor? Send us a message or give us a call (888)616-9885 – we know a lot of local realtors in the states we are licensed in and we are more than happy to help connect you.

Don’t forget to create a list of all your wants and needs in a home. Download our Home Comparison Checklist to take with you as you go to Open Houses. This checklist identifies important factors to consider when choosing a home. It will help you to evaluate the features of up to 3 homes in a side-by-side comparison including tings like neighborhoods, the layout of each home, home exterior, utilities and maintenance. Click here to download your free checklist.

#3 Research, Research, Research!

Did we say research? Make sure to do you research. Your Real Estate Agent will have access to information about what homes have sold for in the past to ensure you don’t over pay. You can also research the home listing to see how long it has been on the market for. If it’s been on the market for quite some time, there may be room to negotiate a lower offer. Speak with your Real Estate Agent! Also, if you’re buying a property with HOA fees, find out if the average annual dues increase. It’s important to know how much you’ll owe so you can factor that into the affordability of the house.

#4 Earnest Money Deposit

Earnest Money deposit, also known as a good faith deposit, is a sum of money you put down to demonstrate your seriousness about buying a house. In most cases, it acts as a deposit on the property you're looking to buy. You deliver the amount when signing the purchase agreement or the sales contract. Speak with your Greenway Loan Officer for more information.

#5 Consider Contingencies

When buying a home, certain conditions must be met by the buyer or seller before closing. They offer protection to the homebuyer. The seller can request concession in the home price negotiation process as well. Contingencies include things like:

- Home Inspection

- Financing

- Appraisal

- Title

- Home Sale

#6. Making an Offer

Your real estate agent will write you offer and submit to the seller’s agent which will be presented to the seller. In you offer make sure to include contingencies, waived contingencies, earnest money amount if applicable, property address, buyer, and seller names, offer price, down payment amount, list of fees and closing costs, date you would like to move into the home, etc.

#7 The Waiting Game

Once you make an offer on a home, the waiting game begins! If the seller accepts your offer as-is, the purchase and sale agreement becomes legally binding! Congrats on your new home.

Keep in mind these scenarios as well:

- The seller can also reject the offer you made without a counteroffer. They do not need is disclose to you the reason why either.

- If the seller makes a counteroffer, you can either accept it, decline it, or counter their counteroffer.

Be sure to speak with your Real Estate Agent so you can come up with the best course of action!

#8: Home Inspections Matter!

A home inspection is very important when buying a new house. A home inspection will come after you’ve made an offer which the seller has accepted. Getting an inspection ensure you know what condition the house is in to avoid costly surprises down the road. While it varies by state, here are some things inspections generally look for:

- Plumbing/electrical issues

- Roof condition

- Exterior rot or decay

- HVAC/heating system issues

- Structural concerns (like foundation)

#9. Congratulations On Your New Home

If the seller accepts your offer, your contract will then be finalized. Each party will then sign the sales contract. The Real Estate Agent will also provide your Loan Officer with a copy of the sales contract and an appraisal report will be ordered. Soon you’ll be moving into the home of your dreams.

Helpful Resources

- First-Time Home Buyer Guide

- Home Comparison Chart

- First-Time Buyer Programs

- Loan Products

- Get Pre-Approved

- Mortgage Calculators

- Contact Us

.png)

5 Biggest Questions This Holiday Season About Real Estate & Mortgages

As we gather with family and friends this holiday season you know what that means. There’s going to be lots of talk about the real estate market, mortgages, and interest rates; especially if you have an aunt, uncle, mother, father, cousin, or friend who’s house hunting.

There’s a lot of speculations about what’s going on and what the future holds. In today’s blog we want to take a few minutes to educate you on what’s really happening. So, sit back and get cozy, we’ve got the answers to 5 of the most popular questions in real estate and mortgages this holiday season.

Question #1: What Will Happen with Home Prices?

If you listen to the news often or read media headlines the housing market and our economy is probably top of mind. While no one has a magic ball to forecast the future, there is data and experts who can provide some insight.

Without a doubt homes are staying on the market longer than they were before. The days of a large influx of new listings is over. Experts say it’s still a seller’s market. Why? Because prices are driven by supply and demand, and we still have a low supply of homes on the market. This means continued upward pressure on home prices.

Question #2: Will there be a housing crisis?

Redfin sums this question up best: “For those bearish folks eagerly awaiting the home price crash, you’ll have to keep waiting. As much as demand is pulling back, supply is as well. And that’s reducing downward pressure on prices in the short run.”

All in all, some experts are projecting slight appreciation and others are calling for a slight deprecation. In turn, they see relatively neutral or flat home price appreciation for 2023.

Question #3: What’s Going to Happen with Mortgage Rates

This may be the biggest question of all. It’s safe to say we were all spoiled by incredibly low interest rates during the pandemic. Rates have more than doubled in less than a year, something that has never been seen before. According to Keeping Current Matters, the average monthly mortgage payment is about $1,000 more than it was a year ago in 2021. Why is this happening? Inflation. The FED has been making moves to help slow the economy and real estate plays a big part in our economy.

George Ratiu, manager of Economic Research at Realtor.com says, “With inflation still running at a 40-year high and the Fed expecting a few more rate increases to combat it, mortgage rates will experience upward pressure through the end of 2022.”

If inflation stays high, so will mortgage rates. When inflation starts to pull back, mortgage rates should too.

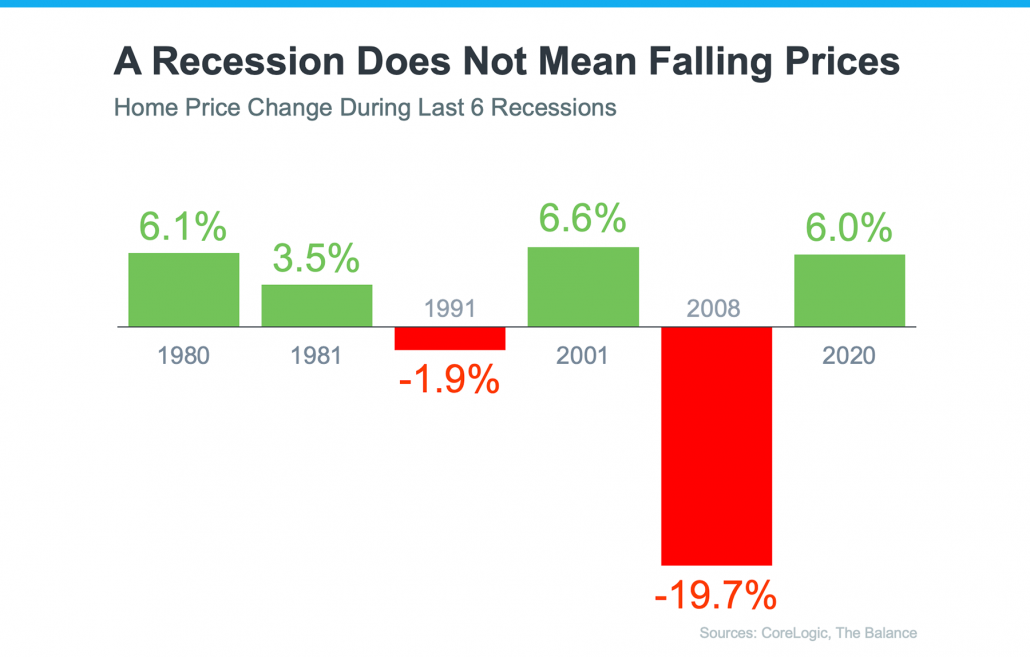

Question #4: If a recession is called, how will it impact the housing market?

First, a recession does not mean falling home prices. In the past 6 recessions, only 2 of them saw a decrease in home prices. A recession may not always cause home prices to fall, but it generally means mortgage rates will.

Question #5: Should I Buy a Home Right Now?

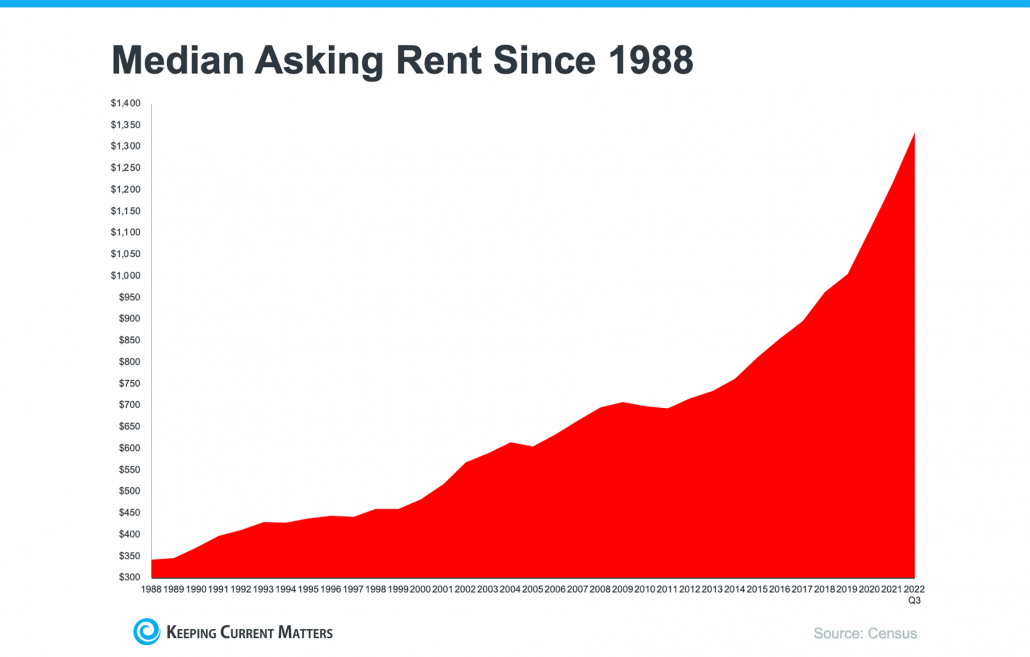

This answer can differ for every home buyer. For instance, first-time homebuyers may want to consider rising rent. Homeownership gives you the chance for a stable monthly mortgage payment all while building wealth. It also offers security and a sense of accomplishment that renting unfortunately cannot.

Another important factor to take into consideration is personal situations. For instance, some jobs may require relocations, aging parents may need to move in, etc. This all plays into whether or not buying a home or selling right now is the right time for you.

Overall, homeownership has many financial and non-financial benefits. The biggest one is that you’ll build wealth.

We’ll leave you with this quote from Odessa Kusi, deputy chief economist of First American, “If you can find a house that meets your financial expectations for a monthly payment and it is a good time for you to buy, then do that…And if you wait for prices to fall and they never do, you may discover the hard way that the house you found a year ago that you really loved, that you could afford but you passed on, is more expensive next year.”

Bottom Line:

There’s no “right” time to buy. Ultimately, the right time is when you are ready. The biggest takeaway is that you shouldn’t let today’s rates keep you from buying a home. Greenway Mortgage offers a variety of loan programs, and we can find one that best fits your financial situation. All it takes is a phone call and review to find out. Reach out and let’s see what might be possible for you today.