The Federal Housing Agency (FHA) has just increased the amount of money that can be borrowed through its mortgage programs by more than $51k in most areas. In high cost locations, the increase is even greater. New limits will take effect in 2023.

The increases will allow more borrowers to take advantage of FHA’s benefits:

- Low down payment options

- Lower total cash-to-close requirements with gift or seller contributions

- More lenient and streamlined refinancing

- Ability to combine purchase and rehab financing

- In some high-cost areas, higher loan limits than conventional mortgages

Here are the specifics:

- In most areas, the FHA loan limit will be $472,030, a 12% increase over 2022’s limit of $420,680.

- In high-cost areas, the limit moves to $1,089,300, a 12% increase over 2022’s $970,800.

- In some lower-cost areas or those with higher costs of construction, limits will vary.

Contact your Greenway Mortgage loan officer today for more details about how the increase can impact you.

New 2023 Loan Limits Effective January 2023

Conforming Loan Limits Increase for 2023

On November 29, 2022, the Federal Housing Finance Agency (FHFA) announced an increase in the maximum conforming loan limits for mortgages acquired by Fannie Mae and Freddie Mac in 2023.

The maximum loan limit for one-unit properties will be $726,000, an increase from $79,000 from $647,200 in 2022. Release.

The decision was based on the recovery of housing prices under the Housing and Economic Recovery Act of 2008 (HERA). They require that the baseline conforming loan limit be adjusted each year for Fannie Mae and Freddie Mac to reflect the change in the average U.S. home price.

FHFA third quarter 2022 House Price Index (HPI) reported that house prices increased 21.21%, on average, between the third quarters of 2021 and 2022. The baseline maximum conforming loan limit in 2023 will increase by the same percentage.

For areas in which 115 percent of the local median home value exceeds the baseline conforming loan limit, the maximum loan limit will be higher than the baseline loan limit.

A list of the 2023 maximum conforming loan limits for all counties and county-equivalent areas in the country can be found here.

Contact your Greenway Mortgage loan officer today for more details about how the increase can impact you.

2023 Conforming Loan Limits Effective January 2023

Fed Increases Rates This November

Let's look beyond the Fed rate increase. As expected, the Fed raised policy rates by 0.75% at their November meeting. That's not the most interesting thing.

Investors were hoping the Fed would signal it's ready to ease off the current pace of rate hikes. And that's what happened. The Fed's statement hinted the Committee may pull back to allow time for the economy to feel the impacts of changes, though it's still committed to using rate increases to tame inflation.

As usual, there's no need to assume mortgage rates will rise the same amount as the Fed's rate boost. Other market forces are also at play, and rates often move before the Fed acts, in anticipation of their changes.

What should you do if you want to purchase or access cash from equity?

If this is your time to make a home financing move, don't let rates stop you.

In some areas, bidding wars have stopped, sellers have adjusted their prices and buyers are back in control. The payment to make an acceptable offer on the home you want may not be much different than if you had to pay over asking prices before.

Let's find a way to work within the framework of the current environment. Options like hybrid ARMs, buydowns and HELOCS can help.

Background on the Fed:

-

The Federal Reserve Board (the Fed) controls the federal funds rate and discount rate, which are charges for overnight loans from bank to bank or from the Fed to member banks.

-

The rate was lowered to near zero in March 2020 in response to the pandemic. These historic measures are now being reversed.

-

This is the sixth increase this year.

Don't let interest rates hold you back from making a move or accessing cash. The team at Greenway Mortgage is happy to help you navigate this market. We're still closing loans every day! Reach out if you have any questions.

.png)

Don't let rate news lock you out!

Mortgage rates are trending upward. Does that mean you should wait to finance, refinance or access cash from equity?

Maybe. But maybe not.

Here's a short video to tell you more about the interest rate environment from our perspective.

The thing is, people still have home financing needs, even with rising rates. In many cases, we are able to help.

In all cases, we're able to have an honest discussion about the available options for a particular scenario.

If your current needs include purchasing a new home or accessing cash from equity, let's talk about rates and loan programs that might help you move forward today.

Even if you're not in the market for home financing, our video can help you understand today's rate environment. We hope you'll check it out.

3 Biggest Questions About Real Estate and Mortgages

As we near the end of 2022, the housing market is still in a constant state of shifts and changes. Some bigger or more impactful than others, but the truth remains the same: while we wish we had a crystal ball, we’ll never be able to predict what’s going to happen. However, one thing will always remain constant: people will always need a place to call home.

There are three big questions in real estate and in the mortgage industry right now. We’ll cover them here. So, before you hit the panic button, give this a read!

Will Mortgage Rates Continue to Rise?

To answer this question, it’s important to understand the why behind the reason mortgage rates have doubled since the beginning of the year and that’s due to inflation.

To ease inflation, the Federal Reserve is taking steps to tame inflation by slowing the economy. In turn, these decisions have an impact on mortgage rates. Until this is under control, we may continue to see rates stay high or rise even higher.

Despite the high mortgage rates, there is still opportunity in the real estate market.

“There is no doubt that the increasing mortgage rate will make homebuying even more challenging, . . . buyers may still find opportunities, as these changes coincide with the time of the year when buyers have historically found the best market conditions to obtain more bargaining power,” said Jiayi Xiu, economist for realtor.com.

What Will Happen to Home Prices?

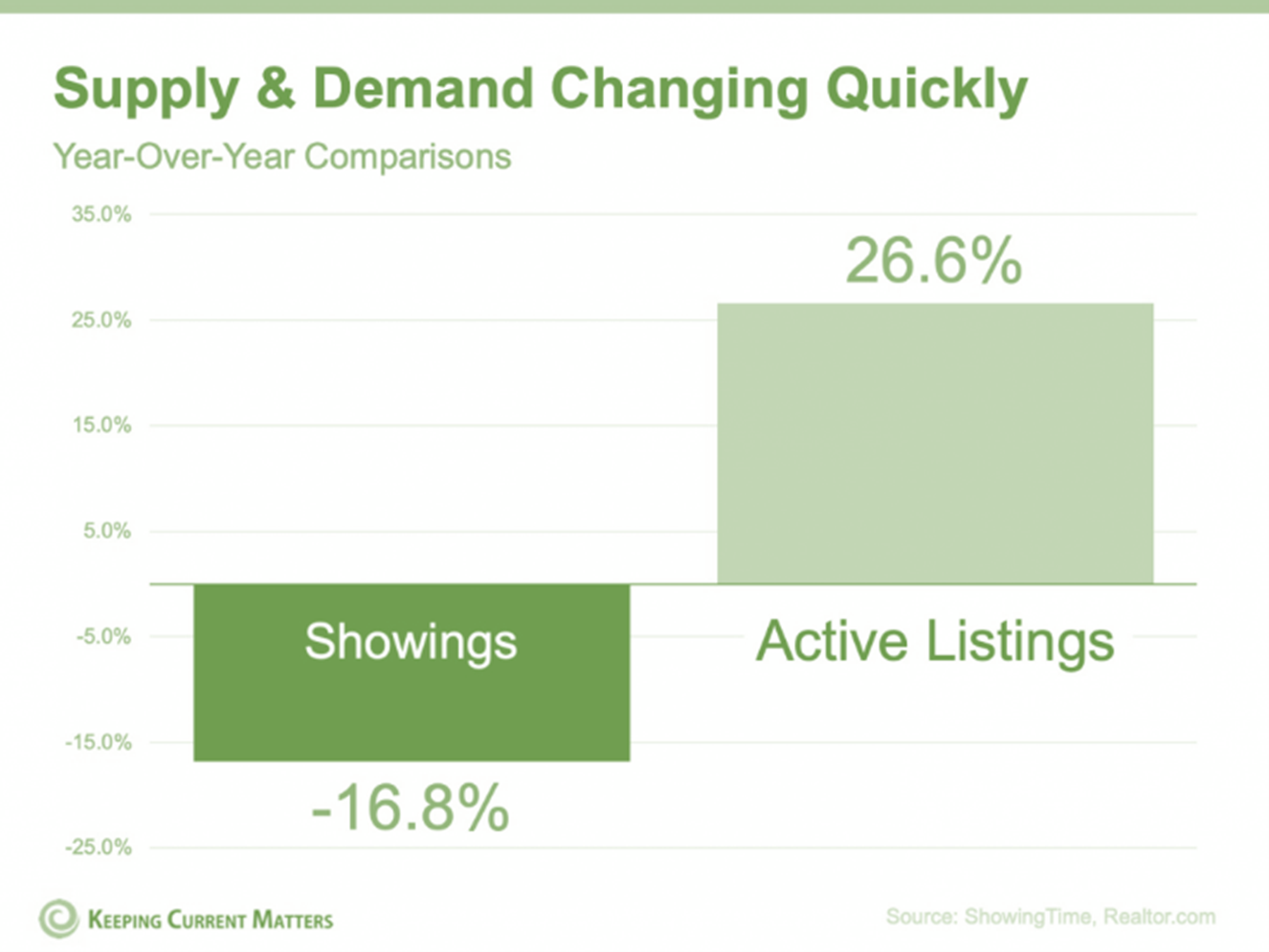

Dave Ramsey sums it up: “The root issue of what drives house prices almost always is supply and demand.”

And when you look at the graph below, you’ll see why we have seen such a large slowdown in home price appreciation in the last few months.

The sudden uptick in mortgage rates and lingering inflation has changed the playing field in the housing market. So, as the pace of sales slows, the more active listings there are. That does not mean we’ll see national deprecation in home values.

Overall, experts are projecting continued price appreciation in most markets, averaging about 1.8% in 2023. However, there are some overheated areas where experts are projecting slight depreciation, but certainly not enough to call it a crash.

Should I Buy A Home Right Now?

Homeownership has many financial and non-financial benefits. It’s true that it costs more to buy a home today than it did last year, but the same is also true for renting. This means, either way, you’re going to be paying more.

Although affordability is challenging right now, buying a home helps you gain equity will will help grow your net worth.

The best way to answer this question is that homeownership will always win over time. It’s a long game.

You can choose to put your money over time into rent and not get a return or play the long game, invest in homeownership and benefit from your investment.

Bottom Line:

As we said before, we wish we had a crystal ball to predict what’s going to happen with mortgage rates or price appreciation, but we unfortunately can’t control that.

Remember, the team at Greenway Mortgage is always here to help answer any questions you have. We are happy to sit down with you to discus which home buying option best suites your scenario and find out how much home you can afford. We’re here to help.

Here are some helpful resources:

- Loan Products

- First Time Home Buyer Resources

- Mortgage Calculators

- Get Pre-Approved

- Apply Now

- Contact Us

.png)