Mortgage News Announcement | Beat the Rush on a Refi

In mid-August, Fannie Mae and Freddie Mac imposed an “adverse market conditions” fee on conventional refinance transactions equal to one-half of one percent of the loan amount causing an industry uproar and spike in rates.

Last week, they offered a short reprieve by delaying the fee until December 1st. However, this fee will likely begin to impact refi rates well before since lenders cannot be certain if a loan will be delivered before the deadline.

Rates are currently near all-time lows but will trend higher as the deadline nears. It is imperative to start the process as soon as possible and get your file in queue before volume leads to longer turn-times.

If you are interested in saving money each month; accessing cash from your home’s equity for any reason; or shortening your loan term, please reach out as soon as possible to discuss your scenario.

December may seem far away, but a lot of interested homeowners are likely to pursue a refinance before the fee increase, and the sheer volume may lead to delays. It’s wise to get started now.

.jpg)

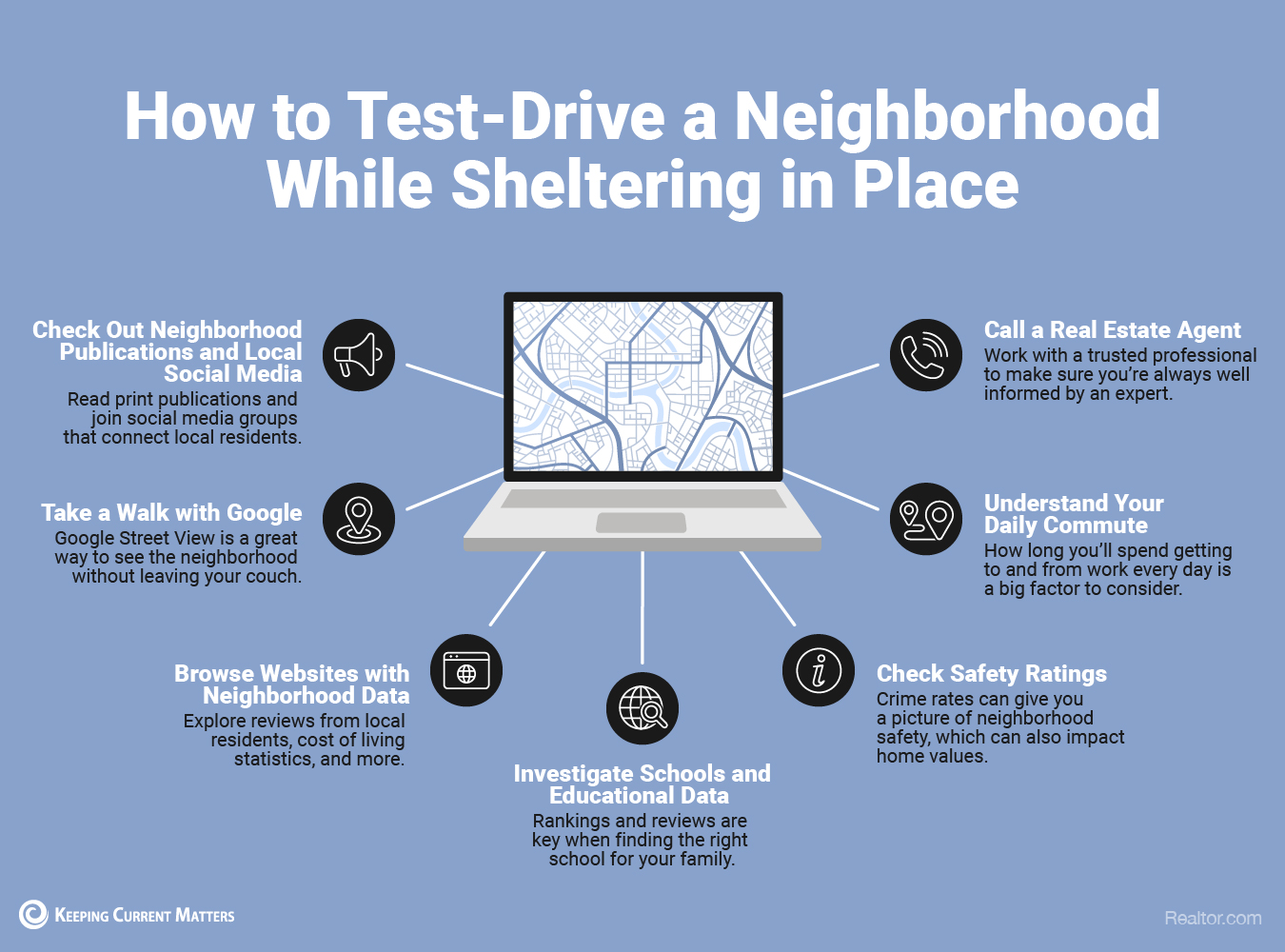

How to Test-Drive a Neighborhood While Sheltering in Place

Staying at home doesn’t mean your search for a new place needs to come to a standstill.

Check out these tips on how to explore other neighborhoods virtually in the homebuying process. You may find a spot that better suits your needs without ever leaving your living room!

#1 - Check out neighborhood publications and local social media

An active neighborhood community will sometimes have a print publication or local social media groups that connect residents. These can provide information on local events and activities that will give you a better feel for the neighborhood. In addition, you can also browse Facebook, Twitter, and Instagram for groups or accounts that document what's going on in the neighborhood where you're interested in moving. Try interacting with locals in the community who can give you their opinions of their locale.

#2 - Take a Walk with Google

Stroll around your potential new neighborhood without leaving the couch! It's easy. Google street view is a great way to view the street and neighborhood virtually. You can access Google Street View by clicking here. Each listing on realtor.com features a link to the Google Street view for that address as well.

#3 - Browse Websites with Neighborhood Data

Gather as much information as you can on your next neighborhood. There are many websites that can help you! City-Data provides detailed city profiles about everything from cost of living to weather to average home prices. Plug in your ZIP code to AreaVibes to get a livability score. This will he you narrow down the best places to live. Yelp provides not only reviews on local cafes, restaurants, and nightlife, but also unfiltered reviews from local residents.

#4 - Search other Real Estate Listings

If you want to learn about the typical architectural styles and ages of home in a neighborhood, browse online listings on sites like realtor.com.

#5 - Call a Real Estate Agent

A real estate agent can help by using technology to test-drive the neighborhood for you. Once you've found a home you're interested in, get in touch with your agent for more information on the neighborhood. They will have a insider's perspective on the area and knowledge on home there too.

#6 - Investigate Schools & Educational Data

Areas with good schools typically maintain property values, and its neighborhoods are high coveted.

#7 - Check Crime Rates

Safety is a priority for both buyers and renters, and crime rates can give you a picture of how safe or dangerous a neighborhood is. Low crime rates are not only safer but can also help keep property values high.

8- Plan Daily Commute

Get a feel for the neighborhood by monitoring traffic and your work commute. You can use tools like Waze or Google Maps which will help predict the level of traffic during your commute hours.

A real estate professional can help you with all of the additional steps along the way, so you’re ready to make your next move. Be sure to get in touch with Greenway Mortgage for all your home financing needs.

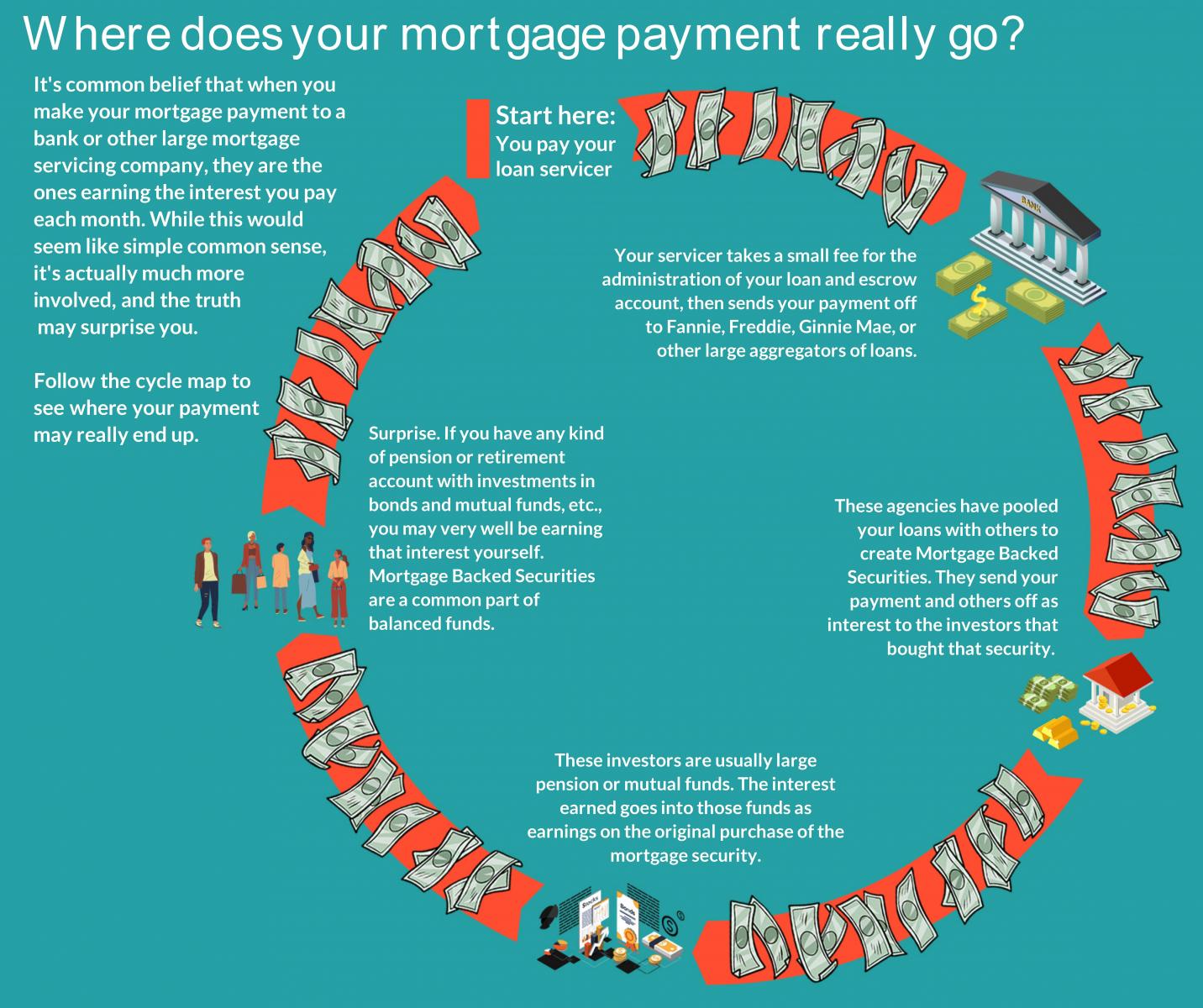

Where Does Your Mortgage Payment Really Go?

Next, your servicer takes a small fee for the administration of your loan and escrow account, then sends your payment off to Fannie, Freddie, Ginnie Mae, or other large aggregators of loans.

These agencies have pooled your loan with others to create Mortgage Backed Securities. They send your payment and others off as interest to the investors that bought that security.

These investors are usually large pension or mutual funds. The interest earned goes into those funds as earnings on the original purchase of the mortgage security.

Surprise. If you have any kind of pension or retirement account with investments in bonds and mutual funds, etc., you may very well be earning that interest yourself. Mortgage Backed Securities are a common part of balanced funds.

Protect Your Credit During COVID-19

Your credit is one of the most important items when it comes to your financial health. Even in the best of the times, maintaining healthy credit can be an overwhelming task, let alone during the economic uncertainties related to the COVID-19 pandemic.

What can you do to protect your credit in the months to come? Keep reading to learn what you can do on your own to prepare.

-

How long will my arrangements last?

-

Can it be renewed?

-

Will interest continue to accrue on your account?

Your Mortgage Payment: Help May Be Available. Don't Just Skip Payments

.png)