Fannie Mae’s Credit Scoring Changes Could Help Enhance Homeownership

Fannie Mae and Freddie Mac recently announced a major change to the way they assess credit scores when multiple clients are on a mortgage. This update could help more borrowers qualify for a home.

How do these changes compare to the old guidelines? We’ll discuss this and more in today’s blog.

Credit Scoring Update

With the recent changes, if there are multiple clients qualifying to purchase or refinance a home, Fannie Mae will now average the median credit scores of all borrowers. How is different? In the past, Fannie Mae looked at the lowest median score of all clients on the loan.

Understanding Your Credit Score

When applying for a mortgage or any loan, your lender will pull your credit score.

A credit score is a number that lenders use, along with other information, to determine if someone will qualify for a loan. An algorithm uses data in your credit report to calculate your credit score. Your credit report shows the following information:

- How much you owe 30%

- Length of your credit history 15%

- Payment history 35%

- New credit inquiries 10%

- What kinds of credit you hold such as auto loans, credit cards and lines of credit 10%

Each of these factors carries a certain weight when calculating your credit score. Once the numbers are crunched, you end up with a credit score between 300 and 850. The higher the number, the lower the risk, and the more likely you are to qualify for a loan and a lower interest rate.

3 Credit Bureaus Explained

The whole credit industry is complicated and largely frustrating for the average consumer. What's even more frustrating is the fact that you don’t just have one credit score. You have quite a few of them, and this isn’t common knowledge.

The three main credit bureaus you’ve probably heard of are: Experian, Transunion, and Equifax. It’s important to understand that while most information collected by these three is similar, there are differences. For instance, one credit bureau may have unique information captured on a consumer that is not being captured by the other two, or the same data element may be stored or displayed differently by the credit bureaus.

For example: The FICO scoring system design is similar across the credit bureaus so that consumers with high FICO Scores on bureau "A's" data will likely see a similarly high FICO Score at the other two bureaus.

It is likely the underlying data in the credit bureaus is different and thus driving that observed score difference. However, there can be score differences even when the underlying data is identical. Why? Each of the bureau’s FICO scoring system was designed to optimize the predictive value of their unique data.

Scoring Models Used by the Mortgage Industry

There are many scoring models, but the two main methods are FICO and Vantage. FICO is the scoring model used by the mortgage industry, specifically Revision 9 which was introduced in 2017. FICO9 includes trended data, which is a historical analysis of credit payment “behavior”. Vantage, on the other hand, renders different scores than FICO. This model weighs different aspects of your credit report.

Although services like Credit Karma give you your Vantage score, these scores are not valid for mortgage qualification. The best way to be proactive and ensure the highest credit score possible is to monitor and manage your credit reports as there can be inaccurate information -It’s best to clear up any errors quickly.

Applying For a Loan Today

In the past, if an individual were to apply for a mortgage loan, lenders would take the median, or middle, credit score of the three as the qualifying one when they apply for a mortgage. And, if two borrowers applied for a loan, the lowest median credit score was used to qualify.

With the most recent updates, when two or more people are on a loan, Fannie May will now average the median credit scores of two individuals.

Since Fannie Mae has a minimum qualifying credit score of 620, this new change should help more clients qualify together on the loan, allowing for the use of all incomes to determine what they can afford. In addition, it also helps borrowers who are still working on their credit but may be applying with a co-signer. By averaging the two scores together, this opens the dream of homeownership to borrowers who may not have been able to obtain a mortgage in the past.

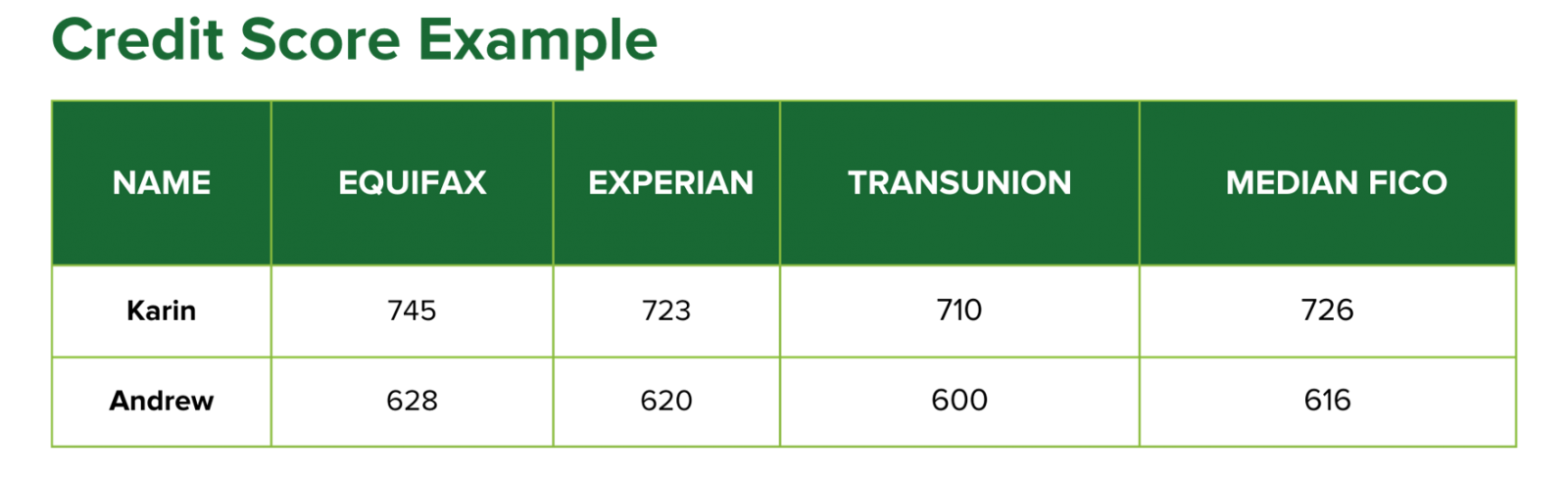

Median Credit Score Example

Let’s look at an example of two borrowers (Karin and Andrew) looking to qualify on a conventional loan together. This chart breaks down each of their credit scores from the three credit bureaus along with their median score.

Karin has a median credit score of 726 while Andrew has a median score of 616. Under the prior guidelines, their lender would not be able to use Andrew’s income on the loan because his median FICO score fell below 620.

However, when both of their median scores are averaged together, the new qualifying score becomes 671. This means both of their incomes and assets can be used to qualify for the loan. This is great news for Karin and Andrew as it allows them to qualify for a bigger loan whether they are looking to buy or refinance.

Conventional Loans vs FHA Loans

There are advantages to both Conventional Loans and FHA Loans.

FHA loans are designed to help first-time home buyers and experienced homeowners alike by providing them with a low-down payment option. It also helps borrowers with less than perfect credit apply for a mortgage.

FHA mortgage insurance serves as a protection for lenders in the event of a homeowner defaulting on their home loan. FHA insured loans often give potential homeowners the option of making a lower down payment than they would need to make if using a traditional, non-FHA insured mortgage.

FHA loans typically have minimum down payments as low as 3.5%. And with this type of loan, you won’t be stuck with mortgage insurance forever. The amount of time you’ll need to pay MIP depends on your down payment. For instance, if you have at least 10% or more, you’ll pay MIP for 11 years. If you put less than 10% down at the closing table, you end up paying for MIP the entire life of the loan.

With Conventional Loans, you can usually request mortgage insurance removal upon reaching 20% equity in your home. There is no upfront premium requirement pad at closing or added to your loan balance.

Bottom Line:

If you have been unable to get qualified for a mortgage loan in the past, now may be a good time to revisit. The new credit scoring changes are opening homeownership up for so many!

Visit our website to check out our Loan Programs or apply online today to get the process started.

Remember, getting pre-approved first is key. Getting an upfront loan approval will help you beat out the competition, negotiate with power and let you know how much you can afford.

Questions? Feel free to give us a call any time 888-616-9885.

We are here to help get you home with customized loan solutions that meet your needs.

Resources:

- How to Manage Your Credit Score

- An Easy-To-Understand Guide to Your Credit Score and The Factors That Influence It

- How Much Can You Save On Your Mortgage By Improving Your Credit Score?

- Credit Score and Mortgage Qualification: What You Need to Know

- Did You Know You Have Multiple Credit Scores?

.png)

Rate Watch: The Fed Increases Rates Again

The Fed again increased rates by 0.25% at their most recent meeting, though some had anticipated a pause in rate hikes. This is the ninth time the Committee has increased rates in the last 12 months.

Here’s why they kept pushing forward.

The Fed statement released after the meeting indicated economic signals, including continuing inflation and the strong labor market, warranted the rate hike, while also expressing confidence in the U.S. banking system. The Committee signaled that some additional rate increases may be appropriate before inflation is brought to the Fed’s target range of 2.0%.

Please Note: Mortgage rates are impacted by market forces beyond Fed actions and will not necessarily change at the same pace as the Fed's moves. They often shift before the Fed acts, in anticipation of changes.

Should the Fed's news change your home financing plans?

If this is your time to purchase or access cash from equity, don't let rates stop you.

Let's find a way to work within the framework of the current environment. Options like fixed rate buydowns, hybrid ARMs, and HELOCS can help

Background on the Fed:

-

The Federal Reserve Board (the Fed) controls the federal funds rate and discount rate, which are charges for overnight loans from bank to bank or from the Fed to member banks.

-

The rate was lowered to near zero in March 2020 in response to the pandemic. These historic measures are now being reversed.

-

This is the ninth increase since March 2022.

Bottom Line

Don't let interest rates hold you back from making a move or accessing cash. Contact us today to take the next step towards homeownership.

.png)

FHA Loan Borrowers Can Soon Save $800 Per Year

Mortgage Insurance will cost less on new FHA home loans. Yes, you heard right, financing a home just became more affordable for hundreds of thousands of buyers!

Beginning March 20, most FHA loans will carry lower mortgage insurance premiums. The average FHA borrower will save $800 per year.* Costs are based on loan amount, so savings will be even higher on pricier homes.

With lower costs, you'll save on your monthly payment and require less income to qualify for the mortgage you want!

Here's a little background:

-

FHA loans can often accommodate borrowers with lower credit scores, income and cash-to-close than conventional loans.

-

FHA loans carry mortgage insurance (MI) as an added monthly cost for the life of the loan (11 years with 10% or more down payment). With this change, MI premiums will fall by 30 basis points, or 0.3% the value of the loan.

-

The reduction applies to all eligible property types, including single family homes, condominiums, and manufactured homes, as well as to all acceptable down payment levels and maximum loan amounts.

If you or someone you know has been unable to qualify for a mortgage due to income or has hesitated because of higher rates, it's a good time to take another look.

Reach out if you want to discuss your situation. We are happy to help.

*Savings are based on the average FHA borrower purchasing a one-unit single family home with a $265,000 mortgage, according to HUD.

.png)

The Fed announced another hike.

As expected, the Fed raised policy rates by 0.25% at their February meeting. This is the smallest increase of the eight made in the last 11 months.

More "interesting" is the Fed's signal regarding future increases.

The Fed statement released after the meeting hinted that ongoing rate increases are anticipated before inflation is brought to the Fed's target of 2.0%. Investors were hoping the Fed would back off of that sentiment.

Please Note: Mortgage rates are impacted by market forces beyond Fed actions and will not necessarily change at the same pace as the Fed's moves. They often shift before the Fed acts, in anticipation of their changes.

Should the Fed's news change your home financing plans?

If this is your time to purchase a home or access cash from equity, don't let rates stop you.

Let's find a way to work within the framework of the current environment. Options like hybrid ARMs, buydowns and HELOCS can help.

Background on the Fed:

- The Federal Reserve Board (the Fed) controls the federal funds rate and discount rate, which are charges for overnight loans from bank to bank or from the Fed to member banks.

- The rate was lowered to near zero in March 2020 in response to the pandemic. These historic measures are now being reversed.

This is the eighth increase since March 2022.

Bottom Line:

Don't let interest rates hold you back from making a move or accessing cash. We're still closing loans every day!

Great News for Homebuyers | New Loan Limits for 2023

There could be savings on the table for home buyers in 2023!

The Federal Housing Finance Agency (FHFA) has just increased the amount of money that can be borrowed through a standard home loan to more than $726K. In some areas, the limit is even higher. The new limits will take effect in 2023.

This is great news for buyers and owners alike.

-

Buyers may be able to borrow more money through a conventional, typically lower-rate loan.

-

Owners may be able to refinance their "jumbo" loan to a lower rate conforming loan and possibly drop mortgage insurance, too.

-

Combining (or avoiding) smaller 1st and 2nd mortgages may now be an option.

-

The increase reflects the growth in values over the past year and reaffirms your decision to invest in a home.

Here are the specifics about the change:

-

The standard loan limit, also known as the conforming loan limit, rose by just over 12% to a maximum of $726,200 in most areas.

-

The percentage increase is equal to the national appreciation average over the last year.

-

This is the 7th year in a row that the FHFA has raised the limit, after a decade of no increases. The limit has risen more than $310K over seven years.

Curious about limits in your county or other areas? Follow the link below to check. We'll update it as limits change, so bookmark it for future reference if you'd like.

If you have questions about what this change could mean for you, please reach out. And if you have friends who may benefit from the news, please pass it along. The Greenway Team would be honored to help them too!