How much do you know about credit scores, how they’re calculated, and what they’re used for? Ramp up your knowledge with this helpful guide so you know what to expect next time you apply for credit.

What’s the Score?

Your credit score is a part of the package of information lenders use to decide whether or not they will lend you money or extend credit. Other factors include things like your employment history and income and their own internal scoring systems.

There are two primary credit scoring models you need to know about: FICO®and VantageScore. Each may be used to determine your creditworthiness: that is, how likely you are to repay your loan. Your score can influence your interest rate, length of loan, and even how much you can borrow.

Calculating Scores

Both scores use a range of 300-850. A higher score indicates to lenders that you are fiscally responsible and the risk of lending to you is low.

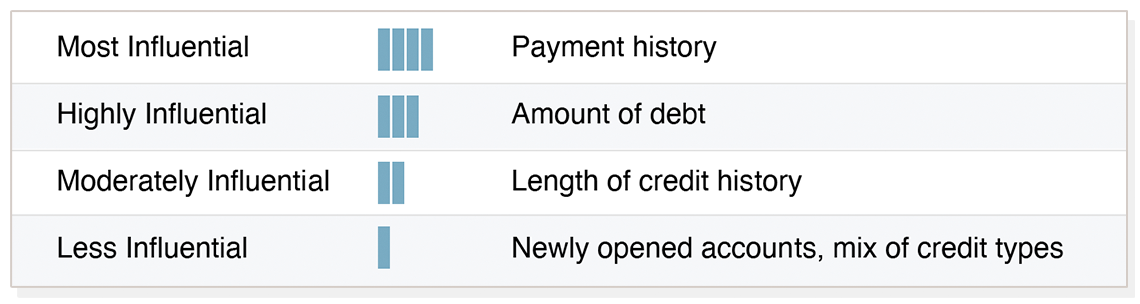

Influences on your FICO Score:

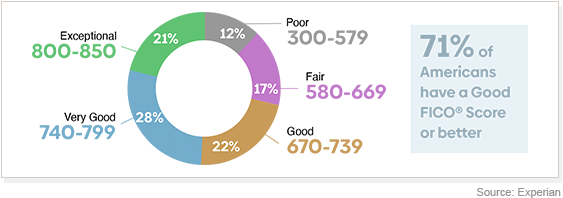

FICO Score Ranges:

FICO Fast Facts:

-

Is not influenced by current interest rates on loans you already have.

-

45-day window for rate shopping before credit is affected.

-

Six months of credit history required to establish a FICO score.

-

Has a separate Auto Score specifically for car loans.

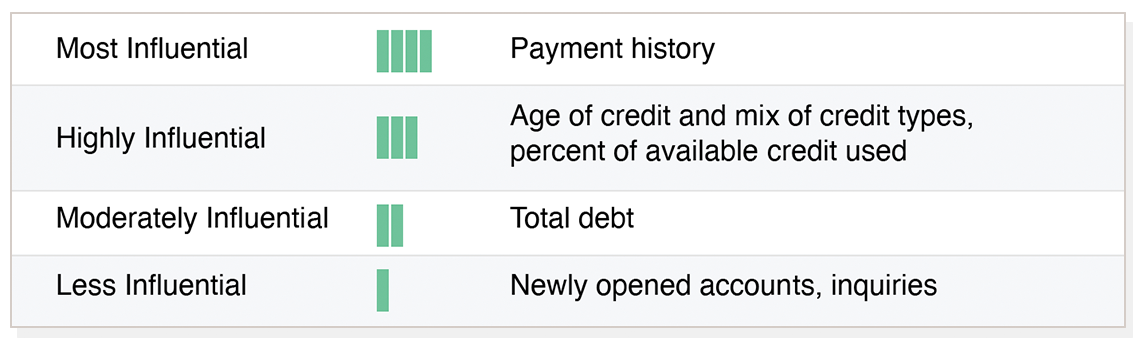

Influences on your VantageScore:

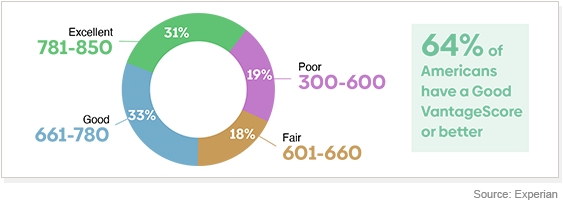

VantageScore Ranges:

VantageScore Fast Facts:

-

Does not factor in paid-off collections when calculating your score.

-

Late mortgage payments are weighted more than other late payments.

-

14-day window for rate shopping before credit is affected.

-

Can produce a score just a month or so after credit line is opened.

What Will My Lender Use?

FICO is used by 90% of lenders and has been around since 1989. (VantageScore only hit the scene in 2006.)

While the FICO Score is currently the gold standard of credit scoring systems, VantageScore is extending its influence throughout the lending industry. Starting in 2025, mortgage lenders will use both VantageScore and FICO when qualifying borrowers for most home loans.*

If you’re not sure which scoring model a lender will use, just ask!

Quick Credit Tips

-

Pay on time, every time. Even if you’re only making the bare minimum payment (but try to pay more!), meeting that debt obligation is key to building good credit.

-

Pay off bills with the highest interest first. You’ll reduce the amount you pay in interest over time, saving you money in the long run.

-

Or, conversely, pay off the smallest bills first. This is the theory behind Dave Ramsey’s Debt

-

Put “bonus” funds toward paying down debt. That includes a bonus from work, a tax refund, or any other lump-sum payment you receive. (But only if you have a savings cushion built up first!)

*Applies to loans backed by Fannie Mae and Freddie Mac. These changes do not apply to government-sponsored loans, including FHA, USDA, and VA loans.

Are you interested in seeing how your current credit score might affect a new mortgage? Let’s take a look together. Give us a call at 888-616-9885 or contact us here!

Confused by Homeowners Insurance? Here’s what you need to know.

Just as you have health insurance to protect yourself and auto insurance for your car, you need the same kind of financial protection when it comes to your home. After all, your home is probably the largest asset you will ever own. Protecting it — and what’s inside — makes sense, but there’s a lot you should know before taking out a new homeowners insurance policy or updating your current coverage.

The Basics of Homeowners Insurance:

Sometimes called hazard insurance, homeowners insurance protects you financially in the event of damage to your home. You can insure not only the physical building but also all the contents and other structures on your property, too. First, though, you have to know what you own so you can determine how much coverage you need. It will also make things easier for you if you need to file a claim. Use this Home Inventory Worksheet to help you catalog your belongings. Fill out as much as you can, and add new purchases to the list as you bring them home. And don’t forget possessions you have in a storage unit, as those items may also be covered by your homeowners insurance.

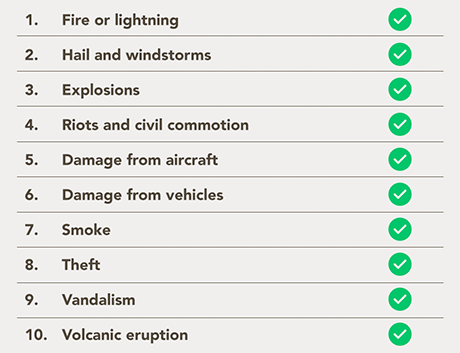

What's Covered: The Perils?*

In general, homeowners insurance policies* will cover 10 basic threats, or “perils,” to your home:

*Insurance rules and regulations differ across states. Exceptions may apply. Texas residents should contact the Texas Department of Insurance for specific information on their state’s requirements.

To help you narrow down which homeowners policy you will need for your home, we’ve listed some of the features of two common homeowners insurance policies. Be sure to consult your insurance agent for more details.

HO2 — Broad form:

This policy will cover the home itself as well as other structures on the property, such as a detached garage or even fencing, but only from the 10 “named perils” listed in your insurance policy. This coverage also provides homeowners with personal liability coverage, which means if someone is injured on your property and then sues you, your insurance company will pay a settlement if you lose the suit, and may also defend you in court.

HO3 — Special form:

This is the most widely used type of homeowners insurance for single-family, owner-occupied homes.2 It covers your dwelling and all attached structures against loss or damage from any peril except for those specifically listed as excluded from coverage, which will likely include flood, earthquake, war, and nuclear accidents, plus whatever the insurance company adds to your policy.3 Your possessions are protected from the 10 named perils, and liability coverage is included. Because an HO3 doesn't limit coverage only to named perils, it often can provide more financial protection than an HO2.

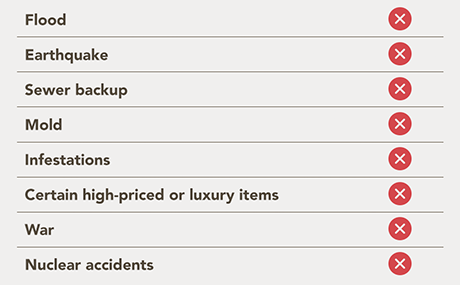

What's NOT Covered by Homeowners Insurance?

There are some things you might expect to be covered by your homeowners insurance, but they actually require a rider or a separate policy. Here are some examples:

A rider is a supplement to a standard insurance policy to cover a specific item or items. An additional premium is required to purchase a rider.

When it comes to what’s covered and what’s not, there are caveats and restrictions for each item that may differ from state to state or between companies, so always be sure you review your policy thoroughly with your insurance agent.

Levels of Coverage:

Let’s look at the levels of coverage you can choose from for your homeowners insurance policy.

-

Cash value. Covers the market value of the home, possessions, and other structures on the property, minus depreciation.

-

Replacement cost. Covers the cost of rebuilding the home with similar materials and replacing possessions, with no depreciation consideration. It’s recommended to insure your home for at least 80% of its replacement value.4

-

Extended replacement cost. Covers the cost of rebuilding and lost possessions and will pay up to a certain percentage over the policy cost. For example, if you have a $100,000 policy, you may be covered up to $125,000. This type of policy provides the most coverage and is the most expensive.5

Note: Full replacement cost policies may not be available for some older homes, as actual replacement or rebuilding of your dwelling is generally not possible. And mobile homes, condos, and historic homes have policies designated specifically for those types of homes.

Homeowners Insurance and Your Mortgage

Most mortgage lenders require borrowers to carry homeowners insurance. After submitting your home loan application, you should begin shopping for coverage immediately. Your chosen insurance company will need to submit information about your policy to your lender. In addition, you’ll need to provide proof of your homeowners insurance at closing. After all, your home is your lender’s collateral in case you default on your loan.

Updating Your Policy:

Just as it’s a good idea to review your home mortgage regularly to ensure it still meets your needs, you should be checking your insurance policy yearly, too. Besides the routine change and flux in our everyday lives, upgrades like installing a pool or updating the kitchen and significant milestones like getting married, having kids, changing jobs, and retiring can influence the coverage you need. Ask yourself what’s changed:

- Did I buy any big-ticket items like antiques or jewelry?

- Do more or fewer people live here than when I took out my original policy?

- Have I renovated or significantly remodeled my home?

A yes answer to any of these questions should have you calling your homeowners insurance agent to set up a meeting.

Nobody wants to think about something unfortunate happening to their home, but the reality is that you need to be prepared in case of that possibility. Homeowners insurance offers that protection. Contact us if you need a recommendation to a local insurance agent.

Sources:

[1] Insurance Information Institute (III), “Which disasters are covered by homeowners insurance?”

[2] National Association of Insurance Commissioners (NAIC), “Dwelling Fire, Homeowners Owner Occupied, and Homeowners Tenant and Condominium/Cooperative Unit Owner’s Insurance Report: Data for 2018.” 2020.

[3] NAIC, “A Consumer’s Guide to Home Insurance.” 2010.

[4] NAIC, Overview of homeowners insurance, “Tips & Tools: Replacement Cost or Actual Cash Value?”

[5] III, “Homeowners Insurance Basics.”

.png&q=95&w=400)

How to Secure a Lower Mortgage Rate & Save Big

Securing a lower mortgage interest rate can make a huge difference in how much you pay for your home over the long haul. Even a small reduction in your rate can save you thousands of dollars over the life of your loan, allowing you to put more money toward other financial goals.

Whether you’re a first-time homebuyer or refinancing your current mortgage, there are strategies you can use to secure a better rate. Here are some tips to help you improve your chances and reduce the overall cost of your mortgage.

1. Maintain a Strong Credit Score

Lenders reward higher credit scores with lower rates. To keep your score in top shape:

✔ Pay bills on time

✔ Avoid opening new credit accounts

✔ Keep existing accounts open (closing them can hurt your score)

✔ Hold off on paying off large loans right before applying for a mortgage

2. Stay Consistent with Employment

Your job history and income stability are key factors in loan approval. Even if a new job offers more pay, switching too soon can delay or complicate your mortgage application.

3. Consider a Larger Down Payment

While some loans allow as little as 3% down, putting more down can:

✔ Help you secure a lower interest rate

✔ Reduce the total interest paid over time

✔ Eliminate the need for private mortgage insurance (PMI) if you reach 20%

Have Questions About Mortgage Rates or the Home Loan Process?

If you’re curious about how a lower mortgage rate could impact your monthly payments or the overall cost of your loan, Greenway Mortgage is here to provide the answers.

Understanding the different factors that influence your rate can help you make informed decisions throughout the mortgage process. Feel free to reach out if you have any questions or need guidance on securing the best rate for your situation.

The Greenway Mortgage team is here to ensure you’re well-equipped to navigate every step of your home financing journey. 888.616.9885

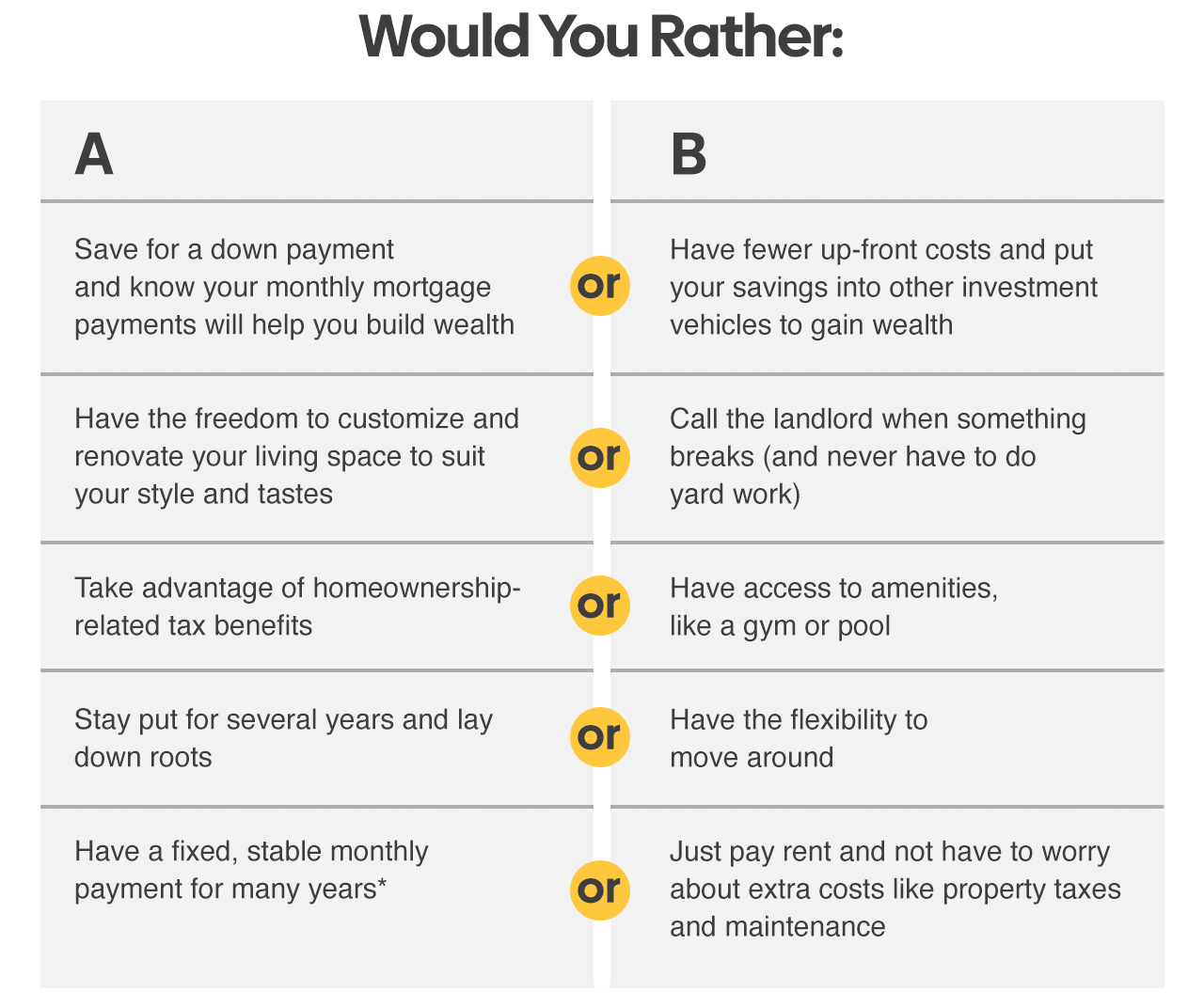

Is Renting or Buying a Better Fit for You? Take This Quiz to Find Out!

Should You Rent or Buy a Home?

Deciding whether to rent or buy a home is a big decision—one that depends on your lifestyle, financial situation, and long-term goals. There’s no right or wrong answer, but this simple exercise might help you find which option feels more aligned with where you are right now.

Take a look at the chart below and think about which options resonate more with your priorities:

What Do Your Answers Say About You?

-

If you answered mostly A’s, homeownership might be the right option for you. It offers stability, the opportunity to build equity, and the freedom to create a space that’s truly your own.

-

If you answered mostly B’s, renting might better suit your lifestyle for the time being. It’s ideal for those who value flexibility and want to avoid the responsibility of property upkeep.

.png)

The Financial Factor: Finances

If you’re considering buying a home, the key question is: Can you afford it? While the benefits of homeownership are significant, it’s important to ensure that it fits into your financial plan.

That’s where Greenway Mortgage can help. Schedule a call to go over your finances and discuss whether you’re ready to take the leap into homeownership. Even if you don’t feel ready just yet, our Loan Officers can guide you through the steps to prepare for the future. 888-616-9885.

Before You Go...Try Our Rent vs Buy Calculator

Ever wondered what you could purchase for the amount you're spending in rent each month?

Use this 𝐪𝐮𝐢𝐜𝐤 𝐜𝐚𝐥𝐜𝐮𝐥𝐚𝐭𝐨𝐫 to see how your rent payment could look as a mortgage—𝙖𝙣𝙙 𝙝𝙤𝙬 𝙖𝙛𝙛𝙤𝙧𝙙𝙖𝙗𝙡𝙚 𝙤𝙬𝙣𝙞𝙣𝙜 𝙢𝙞𝙜𝙝𝙩 𝙖𝙘𝙩𝙪𝙖𝙡𝙡𝙮 𝙗𝙚.

𝘞𝘩𝘪𝘭𝘦 𝘵𝘩𝘪𝘴 𝘵𝘰𝘰𝘭 𝘪𝘴 𝘨𝘰𝘰𝘥 𝘧𝘰𝘳 𝘮𝘢𝘬𝘪𝘯𝘨 𝘳𝘰𝘶𝘨𝘩 𝘦𝘴𝘵𝘪𝘮𝘢𝘵𝘦𝘴, 𝘺𝘰𝘶'𝘭𝘭 𝘯𝘦𝘦𝘥 𝘵𝘩𝘦 𝘬𝘯𝘰𝘸-𝘩𝘰𝘸 𝘰𝘧 𝘢𝘯 𝘦𝘹𝘱𝘦𝘳𝘪𝘦𝘯𝘤𝘦𝘥 𝘮𝘰𝘳𝘵𝘨𝘢𝘨𝘦 𝘱𝘳𝘰𝘧𝘦𝘴𝘴𝘪𝘰𝘯𝘢𝘭 𝘭𝘪𝘬𝘦 𝘎𝘳𝘦𝘦𝘯𝘸𝘢𝘺 𝘛𝘦𝘢𝘮 𝘢𝘵 𝘎𝘳𝘦𝘦𝘯𝘸𝘢𝘺 𝘔𝘰𝘳𝘵𝘨𝘢𝘨𝘦 𝘵𝘰 𝘨𝘦𝘵 𝘮𝘰𝘳𝘦 𝘢𝘤𝘤𝘶𝘳𝘢𝘵𝘦 𝘯𝘶𝘮𝘣𝘦𝘳𝘴.

*With a fixed-rate mortgage, the monthly principal and interest payments are fixed. Changes to your taxes and insurance costs may cause your monthly mortgage payment to increase or decrease each year.

**2022 Survey of Consumer Finances

Buying a home is an exciting milestone, but it comes with financial commitments that go beyond the purchase price.

Understanding these costs can help you plan and budget effectively, ensuring you’re prepared for every step of the journey.

Here’s a detailed look at what to expect:

Down Payment and Earnest Money

Before you even purchase the home, you’ll need upfront cash for your earnest money and down payment. While many people believe you must put down 20%, there are loan programs that require much less—as little as 3.5%, or even 0% for those who qualify.

Your Monthly Mortgage Payment

Your monthly payment will typically include these three key components:

-

Principal: The actual amount you’re borrowing.

-

Interest: The cost of borrowing money for your home.

-

Escrow: A third-party account that pays property taxes and insurance on your behalf.

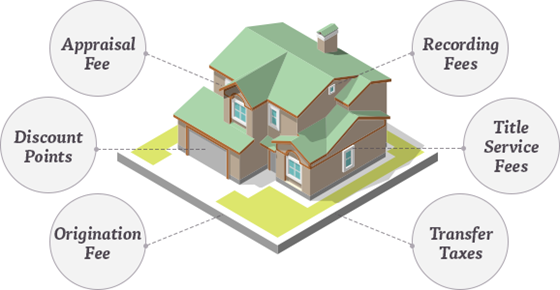

Additionally, you’ll need to account for closing costs—a one-time payment due when your loan is finalized. These costs vary but often include:

-

Loan origination fees

-

Appraisal and inspection costs

-

Title insurance

-

Recording fees

Tip: You can negotiate with the seller to cover some or all of your closing costs. If that’s not possible, let’s discuss the option of rolling these costs into your loan.

Other Expenses to Budget For

Owning a home comes with ongoing expenses and responsibilities. Here are a few you should prepare for:

-

Maintenance and Upkeep: Routine repairs, landscaping, and other upkeep are necessary to protect your investment.

-

Utilities: Monthly bills for electricity, water, internet, and more.

-

Moving Costs: Whether you’re hiring movers or recruiting friends, set aside funds for a smooth transition into your new home.

If you have any questions about these costs or want to explore your financing options, the Greenway Mortgage team is here to help. Contact us anytime. 888-616-9885.