Confused by Homeowners Insurance? Here’s what you need to know.

Just as you have health insurance to protect yourself and auto insurance for your car, you need the same kind of financial protection when it comes to your home. After all, your home is probably the largest asset you will ever own. Protecting it — and what’s inside — makes sense, but there’s a lot you should know before taking out a new homeowners insurance policy or updating your current coverage.

The Basics of Homeowners Insurance:

Sometimes called hazard insurance, homeowners insurance protects you financially in the event of damage to your home. You can insure not only the physical building but also all the contents and other structures on your property, too. First, though, you have to know what you own so you can determine how much coverage you need. It will also make things easier for you if you need to file a claim. Use this Home Inventory Worksheet to help you catalog your belongings. Fill out as much as you can, and add new purchases to the list as you bring them home. And don’t forget possessions you have in a storage unit, as those items may also be covered by your homeowners insurance.

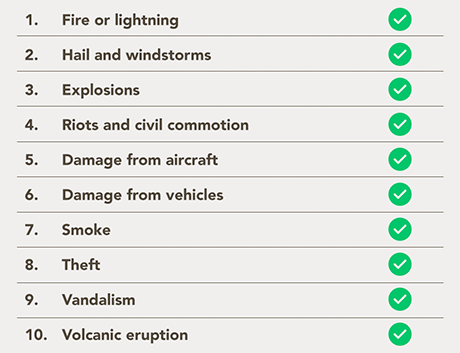

What's Covered: The Perils?*

In general, homeowners insurance policies* will cover 10 basic threats, or “perils,” to your home:

*Insurance rules and regulations differ across states. Exceptions may apply. Texas residents should contact the Texas Department of Insurance for specific information on their state’s requirements.

To help you narrow down which homeowners policy you will need for your home, we’ve listed some of the features of two common homeowners insurance policies. Be sure to consult your insurance agent for more details.

HO2 — Broad form:

This policy will cover the home itself as well as other structures on the property, such as a detached garage or even fencing, but only from the 10 “named perils” listed in your insurance policy. This coverage also provides homeowners with personal liability coverage, which means if someone is injured on your property and then sues you, your insurance company will pay a settlement if you lose the suit, and may also defend you in court.

HO3 — Special form:

This is the most widely used type of homeowners insurance for single-family, owner-occupied homes.2 It covers your dwelling and all attached structures against loss or damage from any peril except for those specifically listed as excluded from coverage, which will likely include flood, earthquake, war, and nuclear accidents, plus whatever the insurance company adds to your policy.3 Your possessions are protected from the 10 named perils, and liability coverage is included. Because an HO3 doesn't limit coverage only to named perils, it often can provide more financial protection than an HO2.

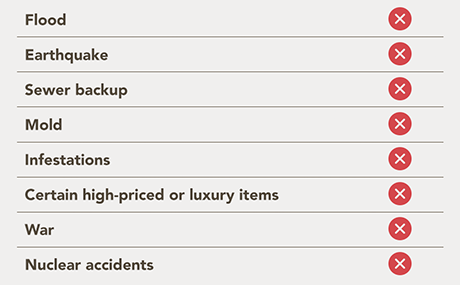

What's NOT Covered by Homeowners Insurance?

There are some things you might expect to be covered by your homeowners insurance, but they actually require a rider or a separate policy. Here are some examples:

A rider is a supplement to a standard insurance policy to cover a specific item or items. An additional premium is required to purchase a rider.

When it comes to what’s covered and what’s not, there are caveats and restrictions for each item that may differ from state to state or between companies, so always be sure you review your policy thoroughly with your insurance agent.

Levels of Coverage:

Let’s look at the levels of coverage you can choose from for your homeowners insurance policy.

-

Cash value. Covers the market value of the home, possessions, and other structures on the property, minus depreciation.

-

Replacement cost. Covers the cost of rebuilding the home with similar materials and replacing possessions, with no depreciation consideration. It’s recommended to insure your home for at least 80% of its replacement value.4

-

Extended replacement cost. Covers the cost of rebuilding and lost possessions and will pay up to a certain percentage over the policy cost. For example, if you have a $100,000 policy, you may be covered up to $125,000. This type of policy provides the most coverage and is the most expensive.5

Note: Full replacement cost policies may not be available for some older homes, as actual replacement or rebuilding of your dwelling is generally not possible. And mobile homes, condos, and historic homes have policies designated specifically for those types of homes.

Homeowners Insurance and Your Mortgage

Most mortgage lenders require borrowers to carry homeowners insurance. After submitting your home loan application, you should begin shopping for coverage immediately. Your chosen insurance company will need to submit information about your policy to your lender. In addition, you’ll need to provide proof of your homeowners insurance at closing. After all, your home is your lender’s collateral in case you default on your loan.

Updating Your Policy:

Just as it’s a good idea to review your home mortgage regularly to ensure it still meets your needs, you should be checking your insurance policy yearly, too. Besides the routine change and flux in our everyday lives, upgrades like installing a pool or updating the kitchen and significant milestones like getting married, having kids, changing jobs, and retiring can influence the coverage you need. Ask yourself what’s changed:

- Did I buy any big-ticket items like antiques or jewelry?

- Do more or fewer people live here than when I took out my original policy?

- Have I renovated or significantly remodeled my home?

A yes answer to any of these questions should have you calling your homeowners insurance agent to set up a meeting.

Nobody wants to think about something unfortunate happening to their home, but the reality is that you need to be prepared in case of that possibility. Homeowners insurance offers that protection. Contact us if you need a recommendation to a local insurance agent.

Sources:

[1] Insurance Information Institute (III), “Which disasters are covered by homeowners insurance?”

[2] National Association of Insurance Commissioners (NAIC), “Dwelling Fire, Homeowners Owner Occupied, and Homeowners Tenant and Condominium/Cooperative Unit Owner’s Insurance Report: Data for 2018.” 2020.

[3] NAIC, “A Consumer’s Guide to Home Insurance.” 2010.

[4] NAIC, Overview of homeowners insurance, “Tips & Tools: Replacement Cost or Actual Cash Value?”

[5] III, “Homeowners Insurance Basics.”