If you’re planning on selling your house in 2022 or if you’re looking to tackle some home renovation projects, we’ve got the top renovations that will give you the highest return on your investment.

Find out what’s trending this year and learn about our Home Renovation Mortgage Loans.

Landscaping

We’re putting this one at the top of our list. You’ve probably heard the phrase a time or two that “first impressions are important”. This is true especially when it comes to selling your home. Curb appeal says a lot about your home, and it offers a tremendous return.

According to HGTV, landscaping is one of few improvements from which homeowners can expect a 100% return on their investment. The average amount spent on landscaping is around $5,000 and most of this is recouped when a home is sold. Since the pandemic, buyers are very interested in outdoor spaces. So, if you’re thinking about sprucing up your outdoor space, we highly recommend doing just that!

Bathroom Remodel

If your bathroom could use some updating, we’ve got some good news. For a midrange bathroom renovation, you could see a 60.1% return on your investment for upgrades like replacing fixtures, adding a ceramic tile bathtub, and a new vanity top according to Bob Vila.

Kitchen Remodel

Kitchens are a huge selling point and one of the most expensive rooms to remodel fully, but a minor kitchen renovation can get you a 72.2% ROI according to Bob Vila. Think about replacing old cabinet doors and drawer front, replacing old hardware, add new countertops and a kitchen sink. If you’re going all out, a full remodel nets only a 57.4% return.

Garage Door Replacements

The garage door is another feature that potential home buyers will notice first. According to an article from BobVila.com, the cost to replace a garage door is around $3,900, which makes the ROI 93.8%.

New Hardwood Floors

Dollar signs start adding up when buyers see flooring they know they’ll need to replace anyway. If you want a top-dollar return, new hardwood floors are key. According to real estate experts, the average ROI for installing hardwood floors is about 70% to 80%, and wood floors can boost the sales price of your home by as much as 2.5%.

New Front Door

Speaking of curb appeal, a new entry door is a crucial part of a home’s perceived value. According to Remodeling Magazine, investing in a new front door has an average ROI of 74.9%.

Window Replacement

Replace your old drafty windows with energy-efficient windows. This can give you an ROI of about 68.6%.

Adding A Deck

Outdoor spaces are a hot item these days! Adding a deck to your home is a smart way to increase your home’s value. According to Bobvila.com, Wood decks are the most popular and net homeowners an average of 66% ROI. If you’ve been longing for a deck, now is a great time to take action!

New Vinyl Siding

Give the exterior of your home the fresh, clean look it deserves. Your house is guaranteed to have the best curb appeal on the block with new vinyl siding. According to Keeping Current Matters, the ROI on new vinyl siding is 63%.

New Roof

If you’ve ever been house hunting before, we’re certain you’ve taken notice of the roof’s condition. Most buyers will push pause on a home if the roof needs to be replaced. It is one of the biggest factors in determining the overall value of a home. According to First Star Exteriors Roofing and Siding, a new roof will likely give you an ROI of about 60-68%, depending on the condition of your old roof and the quality of materials used.

Greenway’s Home Renovation Loans

If a home renovation is on your road map this year, you may want to consider a Home Renovation Loan from Greenway Mortgage. Whether your home improvement projects are large or small, a renovation loan can help you get the job done and it’ll improve the overall value of your home as well.

Although you may be able to pay for home improvements with a personal loan or other types of financing, these methods have higher interest rates and monthly payments.

Instead, you can combine the purchase price plus the renovation costs into one mortgage payment or refinance your existing mortgage plus construction costs into a new mortgage. Our renovation programs make it easy for you to improve your property by including the extra financing in a purchase or refinance loan.

Our Renovation Loans Include:

- FHA 203 K Program

- Streamlined 203K

- Standard 203K

- HomeStyle

If you’re interested in learning more about how a Renovation Loan can help you, contact us today or visit our website here.

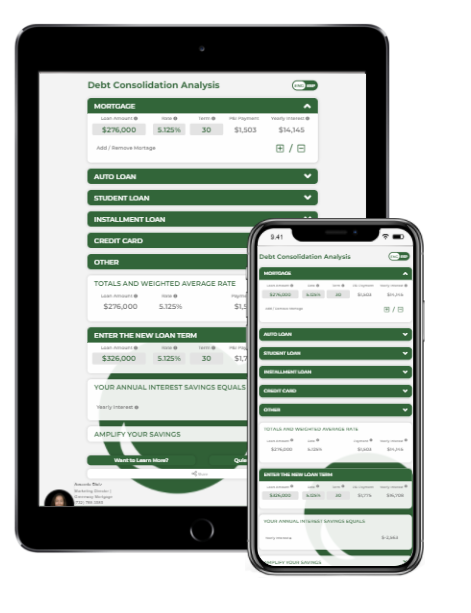

Did you know that interest savings may be hiding in your mortgage?

When you think of a mortgage loan, you typically think of interest costs. But if you consolidate other debts into your mortgage, you can start thinking of interest savings instead.

Most consumer debt carries a higher interest rate than home financing. If you access cash to pay off some of those debts – even at a slightly higher interest rate than your current mortgage – you can still save on overall interest expenditures.

And if you use your monthly savings to pay extra on your principal each month, you can pay off your mortgage faster and save even more.

And if you use your monthly savings to pay extra on your principal each month, you can pay off your mortgage faster and save even more.

Try Our Debt Consolidation Calculator

We have a Debt Consolidation Calculator that you can use to determine how much interest you’re currently paying. In addition, you’ll be able to see how much you can save with a new consolidation loan!

Have Questions About Debt Consolidation?

If you want to talk through your scenario, please reach out to the experts at Greenway Mortgage.

Our team is happy to assist you with any questions you may have!

It's that time of year when many of us start making updates to our homes. May is Home Remodeling Month and Greenway Mortgage is celebrating all month long! Be sure to visit our Facebook and Instagram pages for remodeling inspiration, trends, and information regarding home improvement.

Since the pandemic, homeowners were encouraged to spend more time indoors and since then realized that their homes may no longer fit their needs like once before. Perhaps some of us need more space, or have always dreamed of a home office or gym, maybe an outdoor deck or kitchen for entertaining? Whatever the case may be, our wants and needs have certainly changed.

Many homeowners are happy with their home but know that home improvements can be made. Others may be looking to sell their home in this real estate market and are looking to potentially increase the value of their home. Home remodeling is a great way to improve the overall quality of your home and live a better lifestyle. You may even be able to tap into your home’s equity to pay for projects!

Let’s discuss some of the many reasons homeowners choose to remodel their homes.

#1 Interest Rates Are Low

While rates have increased they are still relatively low compared to historical trends and other loan products which makes it an ideal time to invest in home remodeling.

#2 Modernizing Your Home

Consider replacing cabinets, installing new light fixtures, painting rooms, or upgrading to new appliances.

#3 Energy-Efficient Homes Save Money

Remodels that improve home energy and water efficient will reduce bills. Click here to learn about our Energy Efficient Mortgage Program. Whether you're a homeowner looking to improve your current home or are shopping for a home to purchase, you can use an EEM to make energy-efficient improvements. Changes you make to your home can improve energy efficiency and lower heating/cooling costs.

Program. Whether you're a homeowner looking to improve your current home or are shopping for a home to purchase, you can use an EEM to make energy-efficient improvements. Changes you make to your home can improve energy efficiency and lower heating/cooling costs.

#4 Improve Curb Appeal

The possibilities are endless when it comes to curb appeal. Improvements such as new siding, fresh paint, landscaping, a new front door or mailbox, or a new roof not only improve the first impression of your home, but they increase the home’s value and sales potential.

#5 Outdoor Living Spaces

Expand your home for entertaining! Add a deck, patio, or porch to your home or maybe an outdoor kitchen. These are very on trend for 2022!

#6 Kitchen Remodel

Remodeling your kitchen enhances functionality. Think about adding a new countertop and backsplash or updating worn or outdated flooring.

#7 Bathroom Remodel

A bathroom remodel can improve comfort and add home value. Why not create the refuge you need at the end of a busy day? Think about replacing vanities, installing a new sink or tub, or improving bathroom lighting. Did you know that if you add a bathroom, your home value could increase by twenty percent?

home value could increase by twenty percent?

#8 Accessibility

Redesigning to accommodate future needs to make your home accessible, regardless of age or disability.

#9 Your Home Feels Stale

Sometimes minor remodeling projects is all that it takes. Paint your walls and baseboards and it will instantly feel fresh and clean. This is great for anyone on a budget.

#10 Make Your Basement Usable

Convert your basement into a living, office, or gym space.

Decide If You Need to Remodel Before Selling

If you’re looking to sell your home, take some time to think about what could be improved. For instance, the external appearance of your home is important for raising the value and sales potential. Fresh paint, clean shutters, a new roof, and landscaping are simple ways you can boost curb appeal if you’re looking to sell.

If you’re planning on big remodeling projects, consider the potential return on investment and if those projects are worth it. Some homes do need a kitchen or bathroom renovation, roof repairs, or other major work, but not all of them. In fact, you may be surprised by how well your house could fair in today’s sellers’ market. If you’re thinking of moving, try to avoid over-investing in big renovations if you won’t make the money back in the sale of your home.

Tip: Dig into the market value of your home and compare it to the actual cost of the remodel. A local real estate professional can help you determine your home’s market value. Once you know the value, get a few quotes from contractors on the potential remodel pricing. From here you can decide if a remodel will give you a return on investment when you sell.

Love Your Home and Aren’t Ready to Sell?

Remodeling allows you to customize your home to meet your needs and desires without building a new home or moving and giving up a familiar neighborhood and schools. More than ever, now is the time to take advantage of lower rates before they continue to rise. Why not make your dream home a reality?

Bottom Line:

Home Remodeling can bring many benefits to you, your family as well as your home. Whether you're working on your home and yard or just enjoying the spring, all of us at Greenway Mortgage wish you sunny days ahead! Happy Remodeling Month!

Resources:

- Free Pre-Approval

- Renovation Mortgage Programs

- Looking to tap into your home’s equity? Contact us to discuss your options.

If you’re not following Greenway Mortgage on social media, check us out on Facebook and Instagram.

.jpg)

3 Tips for Single Home Buyers: How to Make Your Dream of Homeownership A Reality

The thought of buying a home on your own as a single home buyer can be intimidating. If you’re making this leap, it’s going to take careful planning and the right team of experts.

Research from Freddie Mac shows 28% of all households (36.1 million) are sole-person, and that number is growing. Over the past 40 years, the number of sole-person households has nearly doubled, and that’s a trend that’s expected to continue as more and more Americans choose to live alone.

“Our calculation suggests that there will be an additional 5 million sole-person households in the United States by the next decade. This means 42% of the household growth will be contributed by sole-person households, . . .”

Do you fall into this category? Here are three tips to help you achieve your homeownership goals.

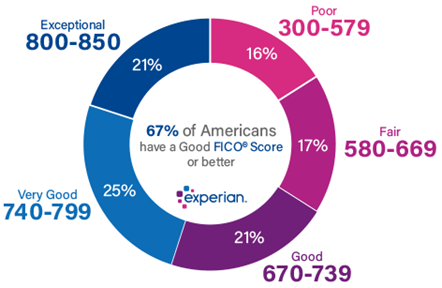

#1 Know Your Credit Score

When you buy a home on your own, you must qualify for your loan based entirely on your finances and credit history. Mortgage lenders will look at your credit profile only so it’s a good idea to review your credit report in advance.

Answer this question here to help you better understand where you may currently stand.

Do you have established credit?

Yes: Great! Keep making those payments on time. Avoid applying for more credit as it will lower your credit score. Every point counts!

No: Start building your credit now. A credit card or secure loan is a great option. But the length of history is important followed by the amounts you owe.

Find out what your score is and see where it falls. If you’re not sure if it’s strong enough or where to focus your energy to improve it, meet with a professional for expert advice on your situation.

#2 Explore Down Payment Options

Your next option is to investigate down payment mortgage programs so you can get a feel for what you’ll need to save to buy a home. Greenway Mortgage offers a variety of down payment programs and first-time homebuyer programs. We’ll see which program best suits your personal needs.

Check Out Some Of Our Programs Here:

#3 Think About Your Future Home and Your Needs

What is it that you want in a home? Here are some questions to ask yourself:

- What type of home do you picture yourself living in?

- What are your wants and needs in a home?

- How many bedrooms and bathrooms do you want?

- Do you need extra space for a home gym, a home office, or for entertaining>?

- Do you want to live in a detached home, a condo, or a townhouse?

While buying a home solo can feel like a big challenge, it doesn’t have to be. If you lean on the professionals, they can help you navigate these waters and make sure you’re able to take advantage of the great opportunities in today’s housing market (like low mortgage rates) to buy your dream home.

Bottom Line

The share of sole-person households is growing. If you’re looking to buy a home on your own, be confident that the dream is achievable. When you’re ready to begin your search, work with the experts at Greenway Mortgage so you have advice each step of the way.

Helpful Home Buying Resources

Check out some of our home buying resources here:

.jpg)

.jpg&q=95&w=400)

Are you a first-time home buyer or thinking about buying a home soon? Greenway Mortgage wants you to feel ready and prepared for the biggest, most exciting purchase of your life. We put together some questions for you to answer so that you can see where you stand currently. Go through and answer each and at the end, if you feel confident and ready, reach out to the team at Greenway Mortgage.

Alright, here we go!

#1 Do you have established credit?

Look below to see where your credit score falls.

If you answered yes, keep making your payments on time. Do not apply for any more credit as it will lower your credit score. Every point counts.

-

Excellent Credit Score: 720-850

-

Good Credit Score: 690-719

-

Fair Credit Score: 630-689

-

Bad Credit Score: 300-629

If you answered no, now is a great time to start building your credit. A credit card or secure loan is a great option. But length of history is important followed by amounts you owe.

#2 How About Your Job?

Two years of employment history is a good rule of thumb. Greenway Mortgage will look at your documented income such as paystubs, tax returns and W2’s.

#3 Have You Been Saving?

You will want to decide how much of a down payment you plan to put down. Keep in mind, that there will be other fees at closing in addition to your down payment. Closing costs can includes fees like:

-

Appraisal

-

Attorney

-

Home Inspection

-

Credit Report

-

Escrow

-

Title

-

Private Mortgage Insurance

-

Property Tax

-

Recording Fees

-

Underwriting & Processing Fees

-

And more

#4 How Much Can You Afford?

It's an important step to determine how much house you will be able to afford. With that said, there is a general rule of thumb that says your total monthly debt – mortgage payments, car payments, credit cards, gas, utilities, etc. – should not exceed 36 percent of your gross monthly income. Lenders typically follow a similar guideline when a qualifying a borrower for a mortgage, although the exact criteria depends on the lender, the borrower and the mortgage program.

The lender qualifies a borrower for a maximum monthly payment that they can afford based on the borrower’s current financial situation, as well as the down payment amount. Remember, your monthly mortgage payment includes PITI – principle, interest, taxes, and insurance.

Second, just because you qualify for a certain monthly payment, that doesn’t mean you should purchase a home that puts you right at that limit or anything close to it. “But wait,” you say. “I’ve crunched the numbers in my monthly budget, and I have no doubt that I can swing that payment with plenty left to spare!”

Are you sure about that?

Do you plan to have kids? Will they go in daycare? If you plan to stay home with your kids, how much income will you lose? Will you start saving for their education? Do you plan to buy a car within the next five years? Would you like to go on vacation? Will this home you’ve fallen in love with require any improvements? In other words, if these or other life events add significantly to your monthly expenses, will you still be able to swing that mortgage payment? Many first-time home buyers become house poor because they buy based on today and fail to consider where they’ll stand tomorrow.

The Better Question to Ask

First-time buyers constantly come to us and say, “How much house can I afford?” Unfortunately, we can’t answer that question with any certainty. We can only tell you how much of a monthly payment you qualify for. The better question to ask is, “How much should I buy?” Again, the lender can’t answer that question. That’s a personal decision you must make based on your income, lifestyle, family situation, and priorities, both now and in the future.

There is no mathematical formula that tells you exactly how much home you could afford. However, Greenway Mortgage will take the time to discuss these issues with you instead of simply approving you for a mortgage and wishing you luck.

Greenway’s online Affordability Calculator can help you get an idea of how much you can borrower from a mortgage lender. Click here to try out our Affordability Calculator.

#5 Did You Know There are First-Time Home Buyer Perks?

Greenway makes buying for the first-time easy! Check out some of our First-Time Home Buyer Programs here.

-

No Money Down FHA Loan: Eligible buyers can get 100% financing towards the purchase of a new home. Learn more about our No Money Down FHA Loan here.

-

NJ FHA Down Payment Assistance Program: Qualified buyers can receive $10K towards down payment. Learn more about our NJ FHA DPA Program here.

-

Conventional 97 First-Time Home Buyer Program: 3% down payment regardless of income levels or geographic location. Learn more about our Conventional 97 First-time home buyer program here.

-

FHA Mortgage: These loans are designed to help first-time homebuyers and experienced homeowners alike by providing them with a low-down payment option. FHA mortgage insurance serves as protection for lenders in the event of a homeowner defaulting on their home loan. Click here to learn more about the FHA Mortgage.

-

HomeReady Program: Designed to help creditworthy homebuyers with limited income in designated areas. Click here to learn more about our HomeReady Program.

You Can Check out all our First-Time Homebuyer Resources here.

First Time Home Buyer Guide

Want to feel prepared before making the leap into homeownership? If so, this eBook is for YOU! You’ll learn how to navigate the entire process from pre-approval to closing and beyond. Click here for your free First-Time Home Buyer Guide.

#6 Feeling Good About Homeownership?

If you’ve made it this far and feel confident, it’s time to schedule an appointment with one of our Loan Experts. Otherwise, hopefully you now know some things you may need to work on based on your current situation. Either way, homeownership is possible! There are many options available to fit your specific needs and the Greenway Team is here to help guide you ever step of the way.

Best of luck on this journey to becoming a homeowner!

.jpg)