New Year, New Home? Understanding how to make an offer on your dream home will be key to getting the best deal possible. And we’ve got the “how-to” guide just for you; and there’s only easy steps to follow. We’ll outline them below.

#1: Get Pre-Approved

First and foremost, step number one should always be getting preapproved. Getting pre-approved is the real deal, especially if you’re serious about purchasing a home.

A pre-approval letter is a statement from the lender that you qualify for a specific mortgage amount based on an underwriter's review of all of your financing information ( credit report, pay stubs, bank statement, assets, salary, etc).

Having that pre-approval letter puts you at an advantage when dealing with a potential seller, as he or she will know you're ONE step closer to getting an actual mortgage. In addition, it will help you beat out the competition, negotiate with power, and let you know how much you can afford so you can start saving for a down payment!

What do you need to get preapproved? Here’s a quick overview of some items you’ll need to gather:

- Pay stubs – last 30 days

- W2s – last 2 years

- Federal tax returns – last 2 years, all pages and schedules

- Bank statements – Last 2 months, all pages

- Realtor and attorney contact info

- Copy of photo ID – must be legible

#2 Find Your Dream Home

Buying a home will be one of the biggest financial purchases of your life. Having a Real Estate Agent by your side will be extremely beneficial. Not only will they be able to help you find the perfect home, but they’ll be able to negotiate the contract and terms as well as make a competitive offer that is within your budget.

Need help finding a realtor? Send us a message or give us a call (888)616-9885 – we know a lot of local realtors in the states we are licensed in and we are more than happy to help connect you.

Don’t forget to create a list of all your wants and needs in a home. Download our Home Comparison Checklist to take with you as you go to Open Houses. This checklist identifies important factors to consider when choosing a home. It will help you to evaluate the features of up to 3 homes in a side-by-side comparison including tings like neighborhoods, the layout of each home, home exterior, utilities and maintenance. Click here to download your free checklist.

#3 Research, Research, Research!

Did we say research? Make sure to do you research. Your Real Estate Agent will have access to information about what homes have sold for in the past to ensure you don’t over pay. You can also research the home listing to see how long it has been on the market for. If it’s been on the market for quite some time, there may be room to negotiate a lower offer. Speak with your Real Estate Agent! Also, if you’re buying a property with HOA fees, find out if the average annual dues increase. It’s important to know how much you’ll owe so you can factor that into the affordability of the house.

#4 Earnest Money Deposit

Earnest Money deposit, also known as a good faith deposit, is a sum of money you put down to demonstrate your seriousness about buying a house. In most cases, it acts as a deposit on the property you're looking to buy. You deliver the amount when signing the purchase agreement or the sales contract. Speak with your Greenway Loan Officer for more information.

#5 Consider Contingencies

When buying a home, certain conditions must be met by the buyer or seller before closing. They offer protection to the homebuyer. The seller can request concession in the home price negotiation process as well. Contingencies include things like:

- Home Inspection

- Financing

- Appraisal

- Title

- Home Sale

#6. Making an Offer

Your real estate agent will write you offer and submit to the seller’s agent which will be presented to the seller. In you offer make sure to include contingencies, waived contingencies, earnest money amount if applicable, property address, buyer, and seller names, offer price, down payment amount, list of fees and closing costs, date you would like to move into the home, etc.

#7 The Waiting Game

Once you make an offer on a home, the waiting game begins! If the seller accepts your offer as-is, the purchase and sale agreement becomes legally binding! Congrats on your new home.

Keep in mind these scenarios as well:

- The seller can also reject the offer you made without a counteroffer. They do not need is disclose to you the reason why either.

- If the seller makes a counteroffer, you can either accept it, decline it, or counter their counteroffer.

Be sure to speak with your Real Estate Agent so you can come up with the best course of action!

#8: Home Inspections Matter!

A home inspection is very important when buying a new house. A home inspection will come after you’ve made an offer which the seller has accepted. Getting an inspection ensure you know what condition the house is in to avoid costly surprises down the road. While it varies by state, here are some things inspections generally look for:

- Plumbing/electrical issues

- Roof condition

- Exterior rot or decay

- HVAC/heating system issues

- Structural concerns (like foundation)

#9. Congratulations On Your New Home

If the seller accepts your offer, your contract will then be finalized. Each party will then sign the sales contract. The Real Estate Agent will also provide your Loan Officer with a copy of the sales contract and an appraisal report will be ordered. Soon you’ll be moving into the home of your dreams.

Helpful Resources

- First-Time Home Buyer Guide

- Home Comparison Chart

- First-Time Buyer Programs

- Loan Products

- Get Pre-Approved

- Mortgage Calculators

- Contact Us

.png)

5 Biggest Questions This Holiday Season About Real Estate & Mortgages

As we gather with family and friends this holiday season you know what that means. There’s going to be lots of talk about the real estate market, mortgages, and interest rates; especially if you have an aunt, uncle, mother, father, cousin, or friend who’s house hunting.

There’s a lot of speculations about what’s going on and what the future holds. In today’s blog we want to take a few minutes to educate you on what’s really happening. So, sit back and get cozy, we’ve got the answers to 5 of the most popular questions in real estate and mortgages this holiday season.

Question #1: What Will Happen with Home Prices?

If you listen to the news often or read media headlines the housing market and our economy is probably top of mind. While no one has a magic ball to forecast the future, there is data and experts who can provide some insight.

Without a doubt homes are staying on the market longer than they were before. The days of a large influx of new listings is over. Experts say it’s still a seller’s market. Why? Because prices are driven by supply and demand, and we still have a low supply of homes on the market. This means continued upward pressure on home prices.

Question #2: Will there be a housing crisis?

Redfin sums this question up best: “For those bearish folks eagerly awaiting the home price crash, you’ll have to keep waiting. As much as demand is pulling back, supply is as well. And that’s reducing downward pressure on prices in the short run.”

All in all, some experts are projecting slight appreciation and others are calling for a slight deprecation. In turn, they see relatively neutral or flat home price appreciation for 2023.

Question #3: What’s Going to Happen with Mortgage Rates

This may be the biggest question of all. It’s safe to say we were all spoiled by incredibly low interest rates during the pandemic. Rates have more than doubled in less than a year, something that has never been seen before. According to Keeping Current Matters, the average monthly mortgage payment is about $1,000 more than it was a year ago in 2021. Why is this happening? Inflation. The FED has been making moves to help slow the economy and real estate plays a big part in our economy.

George Ratiu, manager of Economic Research at Realtor.com says, “With inflation still running at a 40-year high and the Fed expecting a few more rate increases to combat it, mortgage rates will experience upward pressure through the end of 2022.”

If inflation stays high, so will mortgage rates. When inflation starts to pull back, mortgage rates should too.

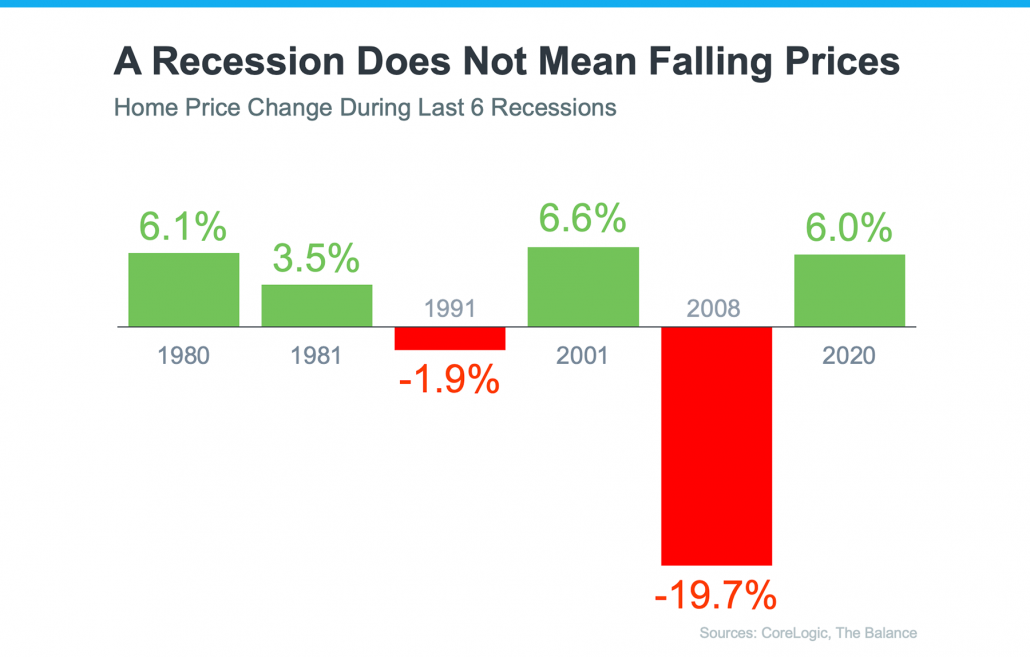

Question #4: If a recession is called, how will it impact the housing market?

First, a recession does not mean falling home prices. In the past 6 recessions, only 2 of them saw a decrease in home prices. A recession may not always cause home prices to fall, but it generally means mortgage rates will.

Question #5: Should I Buy a Home Right Now?

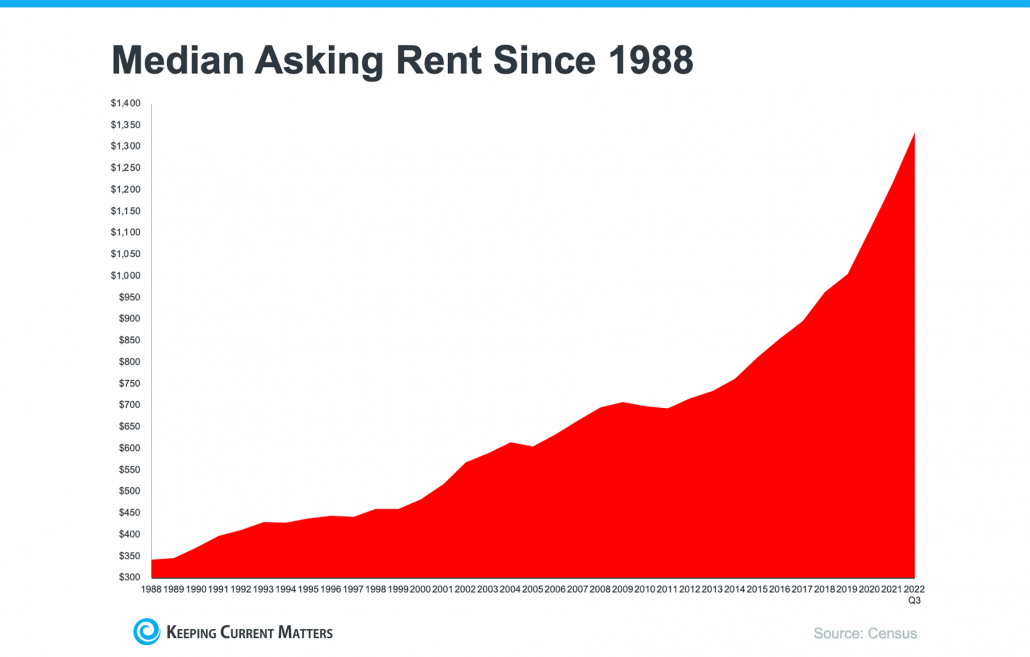

This answer can differ for every home buyer. For instance, first-time homebuyers may want to consider rising rent. Homeownership gives you the chance for a stable monthly mortgage payment all while building wealth. It also offers security and a sense of accomplishment that renting unfortunately cannot.

Another important factor to take into consideration is personal situations. For instance, some jobs may require relocations, aging parents may need to move in, etc. This all plays into whether or not buying a home or selling right now is the right time for you.

Overall, homeownership has many financial and non-financial benefits. The biggest one is that you’ll build wealth.

We’ll leave you with this quote from Odessa Kusi, deputy chief economist of First American, “If you can find a house that meets your financial expectations for a monthly payment and it is a good time for you to buy, then do that…And if you wait for prices to fall and they never do, you may discover the hard way that the house you found a year ago that you really loved, that you could afford but you passed on, is more expensive next year.”

Bottom Line:

There’s no “right” time to buy. Ultimately, the right time is when you are ready. The biggest takeaway is that you shouldn’t let today’s rates keep you from buying a home. Greenway Mortgage offers a variety of loan programs, and we can find one that best fits your financial situation. All it takes is a phone call and review to find out. Reach out and let’s see what might be possible for you today.

Let’s compare the costs and benefits of renting and owning.

If you're choosing between renting and owning, it's important to look past the monthly payment. Renting is sometimes (not always) cheaper by the month. Over time, though, the benefits of owning typically make a purchase a much better deal.

Our Renting vs Owning Calculator will show you how the costs and benefits might compare for your scenario.

When deciding keep in mind these key reasons why so many Americans continue to value homeownership. Let’s take a look at some financial benefits and non-financial benefits to owning a home.

The Financial Benefits of Owning a Home

Owning a home is a huge wealth-building tool and it provides financial stability over renting by locking in your monthly housing payments for the length of your home loans.

An article from Forbes explains: “Understanding the potential benefits of homeownership helps individuals see the value of owning property instead of renting. . . . household wealth among homeowners is a whopping 1,469% higher on average compared to renters, excluding home equity, making the allure of homeownership even more enticing.”

Over time, owning a home helps boost your net worth. It also sets future generations up for success as you pass that wealth down. After all, homeownership is the American dream.

The Non-Financial Benefits of Homeownership

Buying a home is not just a financial decision it’s a lifestyle decision. A few non-financial benefits include things like:

- Freedom and control over your living space

- Giving you a greater sense of pride and purpose

- Helps with community engagement

Bottom Line:

Buying a home is certainly a powerful decision and it’s of the most important and biggest things you’ll do in life. Having a place to call your own and build wealth is what the homeownership dream is all about.

If you have questions about the numbers from our Rent vs Own Calculator, have any general questions, or would like to get started on your purchase, please reach out. The team at Greenway is happy to help!

𝐀 𝐍𝐢𝐠𝐡𝐭 𝐨𝐟 𝐂𝐨𝐦𝐩𝐚𝐬𝐬𝐢𝐨𝐧 𝐄𝐯𝐞𝐧𝐭

Over 270 people attended Halfway Home Animal Rescue Team's 𝐀 𝐍𝐢𝐠𝐡𝐭 𝐨𝐟 𝐂𝐨𝐦𝐩𝐚𝐬𝐬𝐢𝐨𝐧 𝐄𝐯𝐞𝐧𝐭 this year, with over 150 amazing prizes donated!

Greenway's President attented the even in Patterson, New Jersey on Thursday, November 10th. Greenway Mortgage was recognized for their generous contributions made in 2021 as we raised over $30k in just three short days to help animals in need.

𝐀 𝐦𝐞𝐬𝐬𝐚𝐠𝐞 𝐟𝐫𝐨𝐦 𝐭𝐡𝐞 𝐇𝐚𝐥𝐟𝐰𝐚𝐲 𝐇𝐨𝐦𝐞 𝐑𝐞𝐬𝐜𝐮𝐞 𝐓𝐞𝐚𝐦:

“We are proud to say that all the delicious five-course dinner, even down to the butter and creamer on the tables was 100% vegan and cruelty-free, as was every single prize. We are very dedicated to our “be kind to every kind” policy, and no animals are ever harmed to help others.

𝗪𝗲 𝗵𝗼𝗻𝗼𝗿𝗲𝗱 𝘁𝗵𝗿𝗲𝗲 𝘃𝗲𝗿𝘆 𝘀𝗽𝗲𝗰𝗶𝗮𝗹 𝗽𝗲𝗼𝗽𝗹𝗲 𝘁𝗵𝗶𝘀 𝘆𝗲𝗮𝗿, 𝗳𝗼𝗿 𝘁𝗵𝗲 𝗱𝗶𝗳𝗳𝗲𝗿𝗲𝗻𝗰𝗲 𝘁𝗵𝗲𝘆 𝗵𝗮𝘃𝗲 𝗺𝗮𝗱𝗲 𝗶𝗻 𝘁𝗵𝗲 𝗿𝗲𝘀𝗰𝘂𝗲, 𝗮𝗻𝗱 𝘁𝗵𝗲 𝘄𝗼𝗿𝗹𝗱 𝗮𝗿𝗼𝘂𝗻𝗱 𝘁𝗵𝗲𝗺. 𝗝𝗮𝗺𝗲𝘀 𝗣𝗮𝘆𝗼𝗿 (𝗱𝗼 𝘆𝗼𝘂 𝗸𝗻𝗼𝘄 𝗵𝗶𝗺?) 𝗳𝗼𝗿 𝘁𝗵𝗲 𝗶𝗻𝗰𝗿𝗲𝗱𝗶𝗯𝗹𝗲 𝗱𝗼𝗻𝗮𝘁𝗶𝗼𝗻 𝗺𝗮𝘁𝗰𝗵 𝗵𝗲 𝗮𝗻𝗱 𝗚𝗿𝗲𝗲𝗻𝘄𝗮𝘆 𝗵𝗮𝘃𝗲 𝗯𝗹𝗲𝘀𝘀𝗲𝗱 𝘂𝘀 𝘄𝗶𝘁𝗵 𝗲𝗮𝗰𝗵 𝘆𝗲𝗮𝗿.

𝗪𝗲 𝗵𝗼𝗻𝗼𝗿𝗲𝗱 𝘁𝗵𝗿𝗲𝗲 𝘃𝗲𝗿𝘆 𝘀𝗽𝗲𝗰𝗶𝗮𝗹 𝗽𝗲𝗼𝗽𝗹𝗲 𝘁𝗵𝗶𝘀 𝘆𝗲𝗮𝗿, 𝗳𝗼𝗿 𝘁𝗵𝗲 𝗱𝗶𝗳𝗳𝗲𝗿𝗲𝗻𝗰𝗲 𝘁𝗵𝗲𝘆 𝗵𝗮𝘃𝗲 𝗺𝗮𝗱𝗲 𝗶𝗻 𝘁𝗵𝗲 𝗿𝗲𝘀𝗰𝘂𝗲, 𝗮𝗻𝗱 𝘁𝗵𝗲 𝘄𝗼𝗿𝗹𝗱 𝗮𝗿𝗼𝘂𝗻𝗱 𝘁𝗵𝗲𝗺. 𝗝𝗮𝗺𝗲𝘀 𝗣𝗮𝘆𝗼𝗿 (𝗱𝗼 𝘆𝗼𝘂 𝗸𝗻𝗼𝘄 𝗵𝗶𝗺?) 𝗳𝗼𝗿 𝘁𝗵𝗲 𝗶𝗻𝗰𝗿𝗲𝗱𝗶𝗯𝗹𝗲 𝗱𝗼𝗻𝗮𝘁𝗶𝗼𝗻 𝗺𝗮𝘁𝗰𝗵 𝗵𝗲 𝗮𝗻𝗱 𝗚𝗿𝗲𝗲𝗻𝘄𝗮𝘆 𝗵𝗮𝘃𝗲 𝗯𝗹𝗲𝘀𝘀𝗲𝗱 𝘂𝘀 𝘄𝗶𝘁𝗵 𝗲𝗮𝗰𝗵 𝘆𝗲𝗮𝗿.

This generous gift has not only raised much-needed funds to save countless animals but has raised awareness for rescue and has helped build a strong sense of community.

Craig & Pamela Goldman, who donated a house to the rescue, so they will always have a place to call home, and Xander Wittkamp, a young boy who helps his family foster special needs dogs was also honored.”

𝘿𝙪𝙚 𝙩𝙤 𝙩𝙝𝙚 𝙠𝙞𝙣𝙙𝙣𝙚𝙨𝙨 𝙖𝙣𝙙 𝙜𝙚𝙣𝙚𝙧𝙤𝙨𝙞𝙩𝙮 𝙤𝙛 𝙨𝙤 𝙢𝙖𝙣𝙮 𝙬𝙤𝙣𝙙𝙚𝙧𝙛𝙪𝙡 𝙥𝙚𝙤𝙥𝙡𝙚, 𝙤𝙫𝙚𝙧 40𝙠 𝙬𝙖𝙨 𝙧𝙖𝙞𝙨𝙚𝙙 𝙛𝙤𝙧 𝙩𝙝𝙚 𝙖𝙣𝙞𝙢𝙖𝙡𝙨!!

Greenway Gives Back

We believe in giving back. We donate 5% of our annual profits to local and regional environmental groups and causes. We are also active in the communities we lend in. Click here to learn more about Greenway’s Giving Back efforts.

.png)

When interest rates were at historic lows, a typical fixed rate mortgage loan was all most people needed. Now, rates have risen. They’re still below long-term averages, yet appreciably higher than before. And of course, higher interest rates lead to higher monthly payments.

Here at Greenway Mortgage, we recognize the rising rate environment and how homeownership may feel out of reach for some. That’s why we now offer a 2-1 Buydown Program to help counteract the trend towards higher rates.

It’s what everyone’s talking about these days, a 2-1 Buydown. We’re sure you’ve probably heard of it, but you may not know exactly what it means. That’s where we come in.

What is a 2-1 Buydown Loan?

With a 2/1 Buydown, borrowers get a 30-year fixed rate loan with an interest rate that’s temporarily discounted 2% during the first year and 1% the second year by paying an upfront fee at closing. By the third year of the mortgage term, the interest rate reaches the original interest rate on the loan.

Borrowers can ease their way into a home with lower payments that simply step up at the end of the first and second year then remain fixed for the remainder of the loan. Here are the details:

Program Details:

- 1st Year: Interest rate starts at 2% under the locked rate

- 2nd Year: Interest rate is 1% below the locked rate.

- 3rd Year: Loan converts to the locked interest rate.

The Fine Print

- Borrower must qualify for full monthly payment (before buydown rate is applied).

- Third-party contributions are eligible.

- Eligibility requirements, exclusions and other terms and conditions apply.

Example of a 2-1 Buydown

Say you lock in a 5% interest rate, the 2-1 Buydown Program allows you to make monthly payments at a 3% interest rate for the entire first year of your mortgage.

Then, in year two, your payments would be based on a 4% interest rate.

Finally, once you hit year three and for the remaining life of your loan, your payments would reflect your originally-agreed-upon 5% interest rate.

What Types of Loans is a 2-1 Buydown Available For?

2-1 Buydowns are available on conforming fixed products.

- 30-year Fixed Rate Conforming Loans*

- Conventional Purchases | Primary: 1-4 Units, Second Home: 1 Unit

- Conventional Refis | Limited Cash-out

- HomeReady / HomePossible | Purchase Primary: 1 Unit

- FHA, VA, USDA | Purchase Primary: 1-4 Units

- FHA 2nd Home | 1 Unit

*High Balance available Conventional, HomeReady, HomePossible

Who Can Benefit From a 2-1 Buydown?

- Borrowers who may earn more within a few years of obtaining mortgage.

- Borrowers who want to use the savings to reduce bills/debt.

- Borrowers receiving contribution or gifts that will fund the buydown at closing.

How Can a Borrower Benefit from a Temporary Buydown?

- Borrowers will pay less money upfront on their monthly mortgage payments.

- It helps ease borrowers into making monthly payments and it saves you money during the first two years of homeownership.

- Lessens the burned on your wallet with any extra expenses typically associated with moving into a new house (furniture, paint, new appliances, etc.)

Why are we seeing the 2-1 Buydown Program now?

In an environment where interest rates are rising, the 2-1 buydown benefits home buyers by helping them ease into the full monthly payment. It’s especially appealing for first-time homebuyers who are having a hard time purchasing a home in a housing market like we’re seeing today.

Bottom Line

If you’re currently house hunting in this turbulent housing market and need to find solutions to lower your monthly payments, this is a program is worth exploring. The market is shifting, but while it’s influenced by high interest rates and high home prices, borrowers may benefit from a 2-1 buydown.

So, are you interested in purchasing a new home and like the idea of easing into your mortgage payments? Contact the team at Greenway Mortgage to get started.

.png)