June is Homeownership Month: Celebrating the Benefits of Owning a Home

National Homeownership comes around every year in June. This annual celebration shines a spotlight on the significance of owning a home and the countless benefits it brings to individuals, families, and communities. By becoming a homeowner, people get a step closer to the American dream. Let's explore the origins of Homeownership Month, delve into the advantages of homeownership, and showcase some compelling statistics that highlight its positive impact.

The Origins of Homeownership Month

National Homeownership Month started as a week-long celebration of homeownership during the Clinton administration in 1995.

It was not until 2002, that it was officially recognized by the U.S. government to promote the value of homeownership and raise awareness about the opportunities it presents. It serves as a reminder of the American Dream and the importance of having a place to call your own.

Throughout June, various organizations, government agencies, and housing advocates come together to provide resources, education, and support to those aspiring to become homeowners.

What Are the Non-Financial Benefits of Homeownership?

Owning a home brings you and your family happiness, satisfaction, and pride.

- Pride of Ownership: A place to call your own. You’ll be able to customize it according to your likes and personality without anyone telling you how.

- Civic Participation: Homeownership creates stability, and a sense of community, and increases civic engagement.

- Provides Stability and creates a positive environment for families.

- Provides a Safe Place: Owning gives you a sense of security and privacy. Two things that have become very valuable in our lives.

What Are the Financial Benefits of Homeownership?

Buying a home is also an investment in your and your family’s financial future.

- Forced Savings: Your monthly mortgage payment is a form of ‘forced savings’ which builds your net worth with every payment!

- Home Equity: Homeownership builds equity every month. You can use that equity to start a business, pay off debt, send your kids to college and so much more.

- Appreciation: Home prices increase annually which helps to create a safety net.

- Net worth: A homeowner's net worth is 44x greater than renters! This gives you the financial freedom to invest.

- Stability: Rent prices may increase each year. However, a fixed mortgage payment allows you to save for future projects and guard against inflation.

- Tax Benefits: Speak with your CPA to discuss the possible tax benefits homeownership can bring you.

Homeownership Stats

- Homeownership in America is constantly on the move, in-fact, some 65.8% of Americans own a home as of 2022.

- Millennials represent 43% of homebuyers, the highest share of any generation.

- The average age of first-time homebuyers in the US is 36 years old according to the National Associate of Realtors (NAR).

- U.S. homeowners on average have about $270,000 in equity, nearly $90,000 more than they had at the onset of the pandemic according to a CoreLogic report.

Bottom Line:

As we celebrate Homeownership Month in June, let us recognize the tremendous benefits that owning a home provides. From financial stability and tax advantages to a sense of community and personalization, homeownership plays a vital role in shaping individuals' lives and enhancing communities. Let us continue to support and empower individuals on their homeownership journey, creating a brighter future for all.

Home Buyer Resources

To encourage and educate aspiring home buyers, Greenway offers free information and resources. You can visit us online to learn more.

-

FREE First-Time Home Buyer eBOOK – Includes handy resources & checklists

-

First-Time Home Buyer Resources – Learn about our First-Time Home Buyer Programs

-

Home Buying Comparison Chart - Take this chart with you during your home search

-

Buying Your First Home – Learn everything you need to know

-

Refinance Your Mortgage - Get a free loan quote

-

Renovation Mortgage Programs - Put your home improvement plan into action

-

Construction Loans - Can't find your dream home? Build it with a Construction Loan

-

FREE Construction Loan Guide Book - Learn everything you need to know about construction loans and the process

-

Mortgage Calculators – We have an entire library of easy-to-use calculators!

-

Mortgage Terms – Get up to speed on some mortgage terminology

-

When Can You Cancel Your Private Mortgage Insurance? - Find out by using our easy calculator

-

Ready to get started? Apply Now using our online application.

.png)

There’s an important rule of thumb about income when it comes to applying for a mortgage. The numbers you report to Uncle Sam are the numbers lenders will use when making a decision about mortgage qualification.

Many borrowers make the mistake of confusing actual income with reported income. Think of actual income as gross income from full-time, part-time or self-employment, or some combination of the three. This is the total number before you write off any expenses at tax time.

For example, suppose your full-time salary is $70,000 and you make another $20,000 from your side job. Your actual income is $90,000. But that’s not the number we use when evaluating your mortgage application.

Reported Income Is All That Matters

At tax time, your accountant will probably write off work expenses. If you claim $15,000 in unreimbursed expenses for your full-time, salaried position and $5,000 from your side job, the taxes you pay will be based on an income of $70,000. That’s your reported income, which is what lenders care about.

Suppose you use Schedule C (Form 1040) to report your income from the company you run as a sole proprietor. You make $100,000, which sounds great. But you have to invest $30,000 into marketing, equipment, phone and internet in order to make that $100,000. You write off these expenses on Schedule C.

Your actual income is $100,000, but your reported income on your tax return is $70,000. That’s the number Greenway Mortgage or any other lender will use in your mortgage application.

To be clear, we’re not saying you shouldn’t claim every legitimate deduction to reduce your tax burden. You just need to understand that deductions reduce your reported income, which could affect your ability to qualify for a mortgage and your overall buying power.

If you’re thinking about buying a home and your accountant tends to be very aggressive in looking for deductions, discuss this with your Greenway Mortgage loan officer and your accountant, and be careful about the expenses you claim.

Tax Return Numbers Must Match Mortgage Application Numbers

We’ve also had clients who said, for example, they made $70,000 last year. But when we looked at their tax return, we find out that they reported a loss from their business. You can’t then apply for a mortgage, which is likely to be government-sponsored by Fannie Mae or Freddie Mac, and claim that you made $70,000. The government already knows that you reported a loss.

In other words, you can’t say one thing on your tax return and say something else on your mortgage application.

Another common point of confusion is unreported income. Borrowers will come to us and say that they make a lot of cash off the books, whether it involves bartending, landscaping or any other type of work for which they’re paid in cash.

If you don’t report that income to the government, and you don’t pay taxes on it, you can’t use it when you apply for a mortgage. Period.

Mortgage Lenders Should Ask for Your Tax Returns

They should, but not all do. Instead, they ask for information from a W2 or a recent pay stub. But tax returns are the only documents that paint a full and accurate income picture that can be used when evaluating a mortgage application.

This is why a pre-approval carries so much more weight than a pre-qualification. Pre-qualification is based on a phone conversation and gives you a general idea of how much you would qualify to borrow. Pre-approval is based on a thorough review of documentation, including your tax returns, and shows exactly how much you would qualify to borrow.

If you have questions about actual income vs. reported income, or you’re thinking of buying a home, contact us to start the pre-qualification process. And please, have two years of tax returns handy.

.png)

.jpg&q=95&w=400)

Key Points

- May is Home Remodeling Month

- The home improvement industry is flourishing

- Not all home renovations deliver the same ROI

- Top 10 home renovation projects with max ROI (according to Zonda Media’s 2023 Cost vs. Value Report)

- Greenway’s Home Renovation Loans

Happy May and Happy Home Remodeling Month! We’re excited to share with you this some of this year's top 10 home improvement projects that have the highest ROI.

If you’re planning on selling your home in 2023 or if you’re simply looking to do some home renovation projects you’ve come to the right place. With the red hot real estate market, home prices rising, and competition among home buyers fierce, any upgrades you make to your home could go a long way in increasing your home’s value while making it even more appealing to buyers if you’re planning on selling.

The Home Improvement Industry

It’s no surprise that the home improvement industry is flourishing. During the pandemic and even now, Americans have truly learned the importance of “home”. In fact, the total amount spent on home renovations and upgrades soared by nearly 27% between 2020 and 2022, according to TodaysHomeowner.com. We think that says a lot!

Statistics from the Joint Center for Housing Studies of Harvard University (JCHS), show that homeowners spent $337 billion on home improvements and repairs in 2020, $368 billion in 2021, and an estimated $427 billion in 2022. Home improvements are expected to grow even more in 2023 and they will continue to grow as high mortgage rates will entice homeowners to renovate their homes instead of selling.

What Exactly is ROI?

ROI stands for “return on investment" and it is used to measure how much of an investment you could get back when you sell your home. It’s important to note that different home improvements yield different ROIs.

According to DesignerPremier.com, in 2023, a home improvement project’s average ROI is 56%. What does that mean? If a homeowner sells their home, they’ll receive $56 back for every $100 spent on home improvements.

Exterior projects have the highest ROI, some over 100%. Creating outdoor spaces was (and still is) a top priority for homeowners during Covid since many of us couldn’t leave our homes or go on that planned vacation.

Before You Start Your Home Remodeling Project

Before starting any project, you'll want to take into consideration these 3 things.

-

First, the real estate market. If you want to increase your resale value, speak with your local real estate agent. They’ll be able to assess your home to let you know if the improvements you want to make will add value.

-

Second, your budget. Determine how much you can afford before starting any home renovation project.

- Last, decide if you’ll attempt the home improvement project yourself (DIY) or if you'll hire a professional to do the job. It’s important to take all of this into consideration before moving forward especially because hiring a professional can cost a bit more!

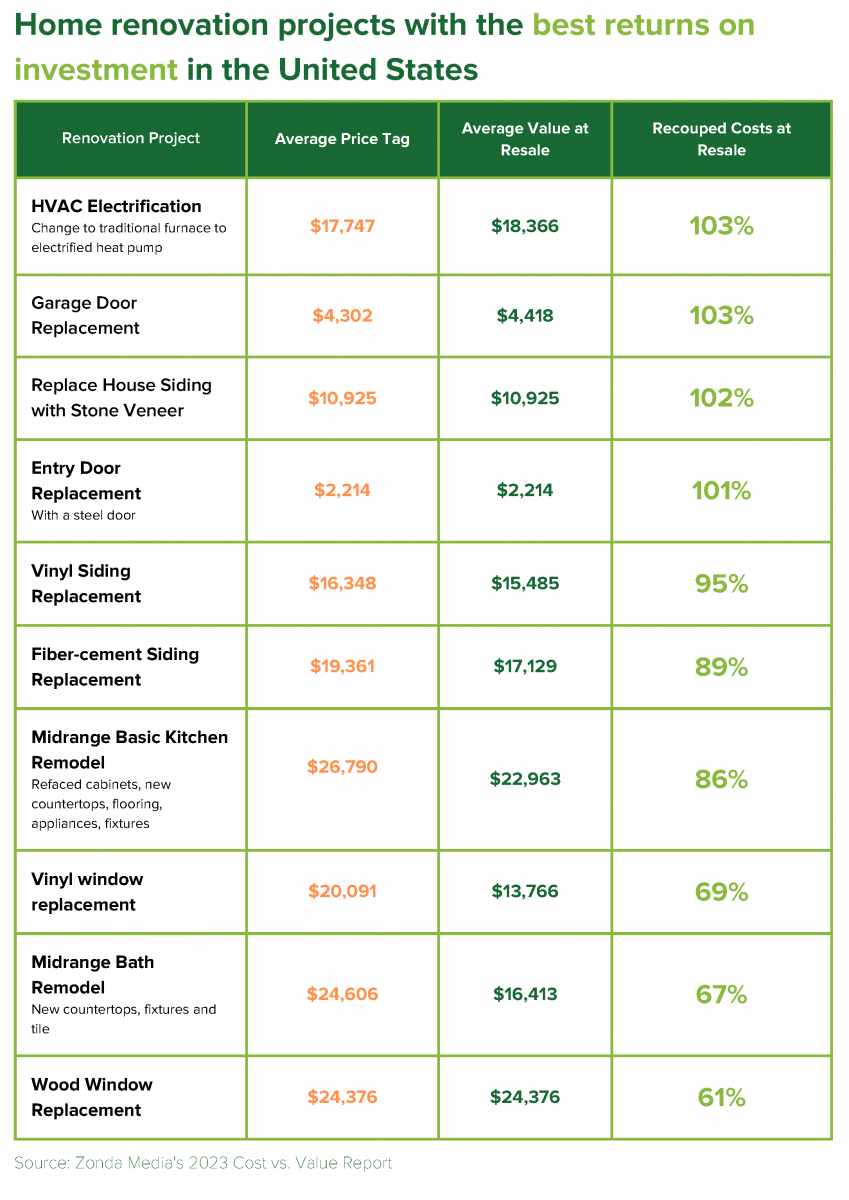

Are you ready to take your home to the next level? Here’s a list of the top 10 home renovation projects that yield that best ROI in the United States.

Source: Zonda Media's 2023 Cost vs. Value report

As you can see, only a few projects could deliver a 100% return on investment like converting a heating, ventilation, and AC system to electric.

Kitchens are a huge selling point and can be one of the most expensive rooms to remodel fully, but a minor kitchen renovation can get you an 86% ROI. If a kitchen remodel is on your list, think about updating the cabinets and countertops, giving your kitchen a fresh coat of paint, or updating the backsplash. Small enhancements like these will provide a high return. Don’t forget the bathroom! A minor bathroom remodel (new countertops, fixtures, and tile) yields a 67% ROI. Major remodels aren't always necessary.

Another easy home renovation project to tackle is the garage door as this is something potential home buyers notice first. Your ROI here is 103%. Need a new front door? A new entry door is another crucial aspect of the home’s perceived value. Investing in a new front (steel) door has an average ROI of 101%.

Replacing old draft windows with new ones can give you a ROI of 69%. A quality vinyl window will also save you money on energy bills because the insulation in the frame of the window itself is energy efficient. Additionally, vinyl windows require no maintenance because they never need painting or scraping. It's clear, vinyl windows give you a great bang for your buck!

Did we mention we offer Energy Efficient Mortgages? Click here to learn more.

Bottom Line:

With home prices on the rise and a tight supply of homes on the market, more people are choosing to fix up their current home rather than looking for a new house.

If a home renovation is on your road map this year, you may want to consider a Home Renovation Loan from Greenway Mortgage. Whether your home improvement projects are large or small, a renovation loan can help you get the job done and it’ll improve the overall value of your home as well.

Although you may be able to pay for home improvements with a personal loan or other types of financing, these methods have higher interest rates and monthly payments.

Instead, you can combine the purchase price plus the renovation costs into one mortgage payment or refinance your existing mortgage plus construction costs into a new mortgage. Our renovation programs make it easy for you to improve your property by including the extra financing in a purchase or refinance loan.

Our Renovation Loans Include:

- FHA 203 K Program

- Streamlined 203K

- Standard 203K

- HomeStyle

If you’re interested in learning more about how a Renovation Loan can help you, contact us today or visit our website here.

.png)

Are you wondering how much you may be able to afford for your home purchase? It pays to know before you look for a home so you can focus on properties that are truly in your comfort range.

How Does Pre-Qualification Work?

Pre-qualifying for a home loan is the easiest way. Here’s how it works. To determine how much you may be able to borrow, we’ll ask questions regarding the source and consistency of your income and savings. We’ll also inquire about any existing debts you may have for cars, credit cards, education, or other types of loans. This is important because not all income can be used to qualify, and any ongoing monthly debts you have will reduce the amount considered available for your housing expenses.

Once we’ve completed the Q&A, we can calculate how much you may be qualified to borrow and how that translates into a comfortable home price. This will be based on:

- Current Rates

- Loan Type

- Down Payment

- Average Tax

- Insurance Rates

Some mortgage payments may also include mortgage insurance or fees for a homeowners association, condominium, or co-op. We’ll take this into consideration too. Keep in mind that qualification factors can vary for different loan programs, and final approval can depend on other factors, such as credit scores and funds to close.

Work With An Experienced Mortgage Lender

With our experience we can help you discover the best programs and strategies to reach your dream home goals. That’s why it’s always worth your while to talk to us before you shop for a home. Want to learn how much home is within your grasp today? Reach out when you’re ready, and we’ll be happy to help.

Helpful Resources

- Loan Programs

- Pre-Approval Request

- Homebuyer Guide

- First-Time Homebuyer Resources

- Meet The Greenway Team

.png)

Did you know that investment funds may be hiding in your mortgage? It's true! You may have more to invest than you think.

A mortgage is the single largest liability most people ever assume. Do your realize its proper management is as important as for any investment?

30-Year vs 15-Year Loan

Which is best the best option? A 30-year or a 15-year loan? Many homeowners want to pay their home loan off as soon as possible, but the value of putting their money into long-term savings and investments often trumps a rapid amortization of principal.

Why pay down the balance on a home loan, only to borrow again later to pay for the kids' college?

The differential savings of a 30-year loan vs. a 15-year option can be put in a 529 plan instead. The result is tax-advantaged growth over time and no uncertainty of borrowing at a potentially high rate later.

Have questions or want to learn more. Reach out! The Greenway Team would love to help and answer any questions you may have.