We are excited to introduce you to Greenway's Community Lending Program, an incentive-based opportunity for eligible properties created to help underserved customers in achieving their dreams of homeownership.

Community Lending Program Highlights

-

Primary Residence

-

Purchase, Rate & Term, Cash-Out Refi

-

Fixed Rate (15, 20 & 30 years), Home Possible/HomeReady (30-year fixed rate only)

-

Not Restricted to First-Time Buyers or Specific Income Levels

THE FINE PRINT

-

Min Credit Score 620 (Purchase & Refi)

-

Min 640 credit score; LTV 95.01 to 97% / CLTV 95.01-105% (where permitted under Agency guidelines)

-

Program eligibility is geographically based and covers a broad economic spectrum

-

No Income limit except specified for the HomePossible or HomeReady products

-

Eligibility requirements, exclusions and other terms and conditions apply

Please feel free to contact us with any questions, to validate a property or to see if you (or your clients) qualify. 888-616-9885.

.png)

Navigating the housing market in 2024 has become increasingly complex, marked by soaring rates, dwindling inventory, and skyrocketing home prices. For first-time homebuyers, saving for a hefty down payment in such circumstances can seem impossible. In February alone, the housing market in New Jersey felt the weight of these shifts, with home prices surging by an astonishing 14.3% year-over-year, while homes sold saw a 1.9% decline, and available listings plummeted by 11.5%, according to data from Redfin.com.

Amidst these challenging circumstances, finding your footing as a first-time homebuyer can seem difficult at times. However, Greenway Mortgage offers a variety of New Jersey First-time Homebuyer programs to help you out when buying a home.

Are you ready to take a closer look at some of these programs?

#1: The Monmouth County, New Jersey First-Time Homebuyers Assistance Program

The Monmouth County, NJ First Time Homebuyer Assistance Program is designed to provide financial assistance to low-income families to purchase an affordable home in the form of a deferred payment second mortgage loan in an amount not to exceed $10,000 for down payment and closing costs (only).

Program Highlights:

- MUST BE a resident of Monmouth County for 1 YEAR before applying for a grant.

- ALL applicants must complete a pre-purchase housing counseling course and provide a certificate of completion with the First-Time Homebuyer application.

- MUST BE an individual(s) that never owned a home (except if an applicant has previously owned a home, he/she still may qualify if they meet 1 or more of the following criteria:

- An individual that has not owned a home in 3 years prior to receiving home assistance.

- An individual who is a single parent even if the individual owned a home with his or her spouse or resided in a home owned by the spouse

- An individual who is a displaced homemaker even if as a homemaker the individual owned a home with his or her spouse or resided in a home owned by the spouse.

The Fine Print:

- Property MUST be the principal residence

- Applicant must purchase a house located in the participating municipalities ONLY.

- Fist-time homebuyer can only purchase a 1-4 family property or condominium unit.

- Housing unit cannot exceed the max purchase price of $337,000 for 1-family & condominium, $432,000 for 2-family unit, $532,000 for a 3-family unit and $648,000 for a 4-family unit.

- Mobile homes are not eligible for purchase using First-time Homebuyer program funds

- Co-signor not allowed

- Eligibility requirements, exclusions and other terms and conditions apply.

For more information and homebuyer eligibility on the Monmouth County, New Jersey First-Time Homebuyers Assistance Program click here.

#2: New Jersey Conventional Down Payment Assistance Program (DPA)

The state of NJ offers a conventional version of their down payment assistance program for first-time homebuyers. Qualified borrowers can receive $15,000 to be used towards down payment and closing with affordable mortgage insurance premiums that follow conventional mortgage guidelines in certain NJ counties*. All other counties will remain at $10,000.

Program Highlights:

- 30-year, Fixed-Rate Conventional Loan

- Affordable Mortgage Insurance Premiums

- $15,000 for Down Payment and Closing Costs*

County List:

- *$15,000 applies to: Bergen, Essex, Hudson, Hunterdon, Mercer, Middlesex, Monmouth, Morris, Ocean, Passaic, Somerset, and Union. Effective November 1, 2022.

- $10,000 applies to: Atlantic, Burlington, Camden, Cape May, Cumberland, Gloucester, Salem, Sussex, Warren.

The Fine Print:

- First-time buyers are borrowers that have not had an ownership interest in their primary residence during the previous three years

- DPA is a $15,000 forgivable loan with no interest and no monthly payments. Forgiven after 5 years as primary residence (While grant funds are available)

- Single-Family Properties and Condos, Owner Occupied, Primary Residence in NJ, Minimum FICO 620

- Income limits are determined by the county of the purchase property but must not exceed 80% of Area Median Income. Please reference the Freddie Mac HFA Income Limits for additional details

- Eligibility requirements, exclusions and other terms and conditions apply.

For more information and homebuyer eligibility on the NJ Conventional DPA Program click here.

#3: New Jersey First-Generation Down Payment Assistance (DPA) Program

This program aims to provide significant assistance for down payments and closing costs to homebuyers, offering a generous $7,000 contribution to those who qualify. When paired with an NJHMFA First Mortgage and the Down Payment Assistance Program, eligible homebuyers can receive up to $22,000 in assistance! The amount varies depending on the county where the property is located.

Program Highlights:

- Owner occupied, primary residence in NJ

- 30-year Fixed-rate mortgage options available for home purchases only

- $22,000 for down payment & closing costs when paired with DPA in certain NJ counties

The Fine Print:

- Must be a first-generation homebuyer

- Min credit score 620; must meet DTI requirements

- Must be paired with an NJHMFA first mortgage loan and the DPA; DPA is a forgivable loan with no interest and no monthly payments

- Single-Family, Condo, Townhome, Co-ops, 2-4 units

- Ineligible for Police & Fireman Program

- Eligibility requirements, exclusions and other terms and conditions apply.

For more information and homebuyer eligibility on the NJ First-Generation DPA Program click here.

Bottom Line:

If you’re a New Jersey homebuyer, take advantage of these homebuying programs so you can achieve your homeownership goals while minimizing your costs. To learn more about these programs and determine your eligibility, click on the links provided or contact us directly at 888-616-9885. We're here to assist and answer any questions you may have.

Click here to connect with a Greenway Mortgage Loan officer today.

.png)

Exciting news. The new enhanced HomeReady program is increasing access to homeownership!

HomeReady® offers an ideal mortgage solution for both first-time and repeat buyers with a low-down payment and flexible financing. To assist very low-income purchase borrowers, Greenway Mortgage now offers a $2,500 credit applicable to down payment and/or closing costs.

The New HomeReady® Program Highlights

-

Borrowers must have a qualifying income of less than or equal to 50% of the applicable area median income of the property’s location.

-

The $2,500 credit must be provided upfront to the borrower and can be applied towards down payment and/or closing costs, including mortgage insurance premiums.

Ideal For:

-

Very low-income individuals

-

First-time or repeat homebuyers

-

Those with limited cash for down payment

-

Supplemental boarder or rental income

What You Need to Know

While HomeReady® offers incredible benefits, it's essential to understand the details:

-

Homeownership Education: If all occupying borrowers are first-time homebuyers, then at least one borrower is required to take homeownership education, regardless of LTV. It’s a small investment in knowledge that can yield significant rewards in your homeownership journey.

-

Act Now: The $2,500 credit is only available until February 15, 2025. Don't miss out on this limited-time opportunity to take advantage of the HomeReady® program.

Eligibility requirements, exclusions and other terms and conditions apply.

Embrace the Journey with HomeReady®

Are you ready to take the next step towards homeownership? Reach out today to see if you qualify or to get pre-approved. The Greenway Mortgage Team is here to guide you every step of the way on your journey to owning your dream home.

Helpful Resources

- Roadmap to Mortgage Pre-Approval

- Homebuyer Guide

- Get pre-approved

- Apply Now – Full Mortgage Application

.png)

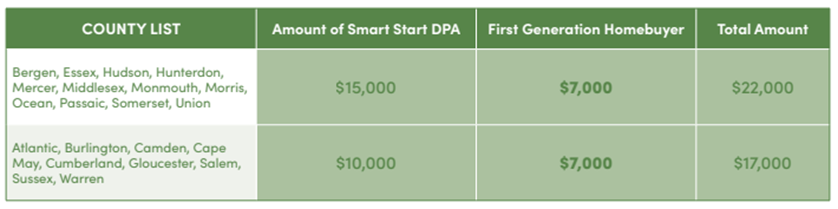

New Jersey Smart Start Plus First-Generation Down Payment Assistance Program

Exciting News for Aspiring Homebuyers in New Jersey!

We’re excited to announce that the state of New Jersey will now offer a new home buying program that’s set to transform the landscape of homeownership, offering an enhanced and more affordable path for first-time home buyers to turn their homeownership dreams into a reality.

Introducing The Smart Start Plus First-Generation Homebuyer Program

Available on October 20, 2023, the Smart Start Plus First-Generation Homebuyer Program is designed to deliver substantial down payment and/or closing cost assistance to qualified homebuyers. Let's delve into the finer details:

This new program extends a generous $7,000 toward down payment and closing costs. But when combined with an NJHMFA First Mortgage and the Down Payment Assistance Program (DPA), potential homebuyers could receive up to an impressive $22,000. The amount varies based on the county where the property is located. For a more comprehensive breakdown, refer to the chart below.

What is DPA?

-

The DPA is a forgivable loan with no interest and no monthly payments for eligible homebuyers purchasing a home in New Jersey.

What is First-Generation Homebuyer DPA?

-

The First-Generation Homebuyer DPA is forgiven if the Borrower resides in the premises as his/her principal residence for five years from the loan closing date and does not refinance or otherwise convey the first mortgage.

Program Details

-

Owner occupied, primary residence in New Jersey.

-

30-year Fixed Rate Mortgage Options Available for Home Purchases Only

-

$22,000 for Down Payment & Closing Costs when paired with DPA in certain NJ counties*

The Fine Print:

-

Must be a first-generation homebuyer**

-

Minimum credit score 620; must meet DTI requirements.

-

Must be paired with an NJHMFA first mortgage loan and the DPA; DPA is a forgivable loan with no interest and no monthly payments.

-

Single-Family Properties, Condo, Townhome, Co-ops, 2-4 units

-

Ineligible for Police & Fireman Program

-

Eligibility requirements, exclusions and other terms and conditions apply.

*Bergan, Essex, Hudson, Hunterdon, Mercer, Middlesex, Monmouth, Morris, Ocean, Passaic, Somerset, and Union Counties.

Who is considered a first-generation homebuyer?

**A first-generation homebuyer is defined as a first-time homebuyer who is either:

A: An individual whose parents or legal guardians do not own any residential property in the United States or abroad, and whose spouse, domestic partner, and household members have not owned a principal residence in the past 3 years in the U.S. or outside of U.S.

OR

B: An individual who has been in foster care in New Jersey at any point.

Bottom Line:

For prospective homebuyers in the Garden State, this program is nothing short of a golden opportunity to secure a brighter future. With greater down payment and closing cost assistance than ever before, this initiative paves the way to homeownership!

Don't miss out on this chance to turn your homeownership dreams into reality with New Jersey's innovative Smart Start Plus First-Generation Down Payment Assistance Program.

Reach out to us today to learn more, confirm your eligibility, or with any questions – we're here to guide you through every step of this exciting journey. Your dream home is closer than you think.

Establishing a line of credit to access your home’s equity is an important decision! You now have a flexible tool you can leverage to fund important endeavors, improve your home, or help support your financial well-being.

How does your HELOC work?

Here are some guidelines for typical HELOCs. If you have an agreement currently, check it for the specifics related to your account.

Spend your cash

Most people find it convenient to access their funds through account transfers or checks.

There are no restrictions on how you spend your funds. If you direct them to home repairs or upgrades, the interest may be tax deductible. Consult your tax advisor to be sure.

Start with interest-only payments

During your initial draw period, which is usually 10 years, you pay only the interest on the funds you’ve borrowed. The rate varies with the market, so you’ll want to keep an eye on your account statements to determine your minimum payment.

If you need help anticipating the payment for a particular expenditure, please reach out. The Greenway Team is glad to help.

You can also pay toward your principal balance if you wish. The amount of the balance you pay down will be available to spend again until the end of your draw period.

Plan for repayment

After your draw period, you’ll begin making fixed principal and interest payments to repay the loan. Repayment terms are typically 10, 15 or 20 years and are spelled out in your agreement.

Remember your HELOC if you sell

If you choose to sell your home while your HELOC is open or in repayment, you will pay off the money you owe at the same time you pay off your mortgage.

If you choose to refinance your first mortgage, the HELOC will either need to be paid off or resubordinated (that simply means it goes back into a secondary lien position—the same as where it started with your existing first mortgage).

Strategies for Leveraging a HELOC For Your Financial Benefit:

BUY a second home or investment property.

Leveraging the equity in your primary home can be a smart way to make the down payment on a vacation home or rental property.

CONSOLIDATE high-rate consumer debt.

Transfer credit card balances to your HELOC to lower your rate and eliminate the stress associated with making multiple payments each month.

LOWER your overall monthly debt payments.

Pay off higher-rate balances more quickly by moving them onto your HELOC then adding the payment amount to your HELOC payment. This prevents extending the term of your other debts.

PAY for higher education.

Give your kids a head start after college by helping them avoid student loans. Use your HELOC to cover tuition, travel, room, board and other expenses.

MAKE home improvements.

A new kitchen, bath, deck or other improvements can make your home more comfortable now and more marketable later if you decide to sell. HELOC funds spent on your home may be tax deductible. Always check with your tax advisor.

There are many ways to make your HELOC pay. If you need help determining what your payments will be after any expenditures, we can help. Please reach out.

.png)