Does it cost more to rent or own?

The answer may surprise you. Many people assume renting is cheaper — but the reality is more nuanced. Comparing housing costs isn’t just about monthly payments. It’s about long-term financial impact, equity, tax benefits, and lifestyle choices.

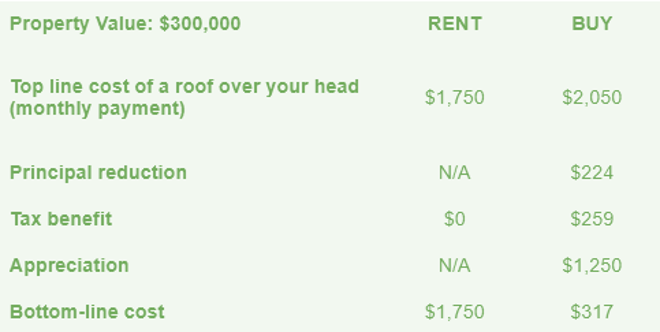

Even with numbers like these some still say renting is better:

-

"Investing in a home is riskier than renting." No risk, no reward. Besides, even studies conducted by the Federal Reserve show that owning can provide a net worth that is from several to hundreds of times greater than that of renters.*

-

"Home values aren't stable." While home prices can drop during some real estate cycles, values have proven to rise over time. The 50-yera average appreciation rate is just over 5% annually.

-

"The tax deductions aren't worth it." Some people benefit from claiming deductions for mortgage interest and real estate taxes. Others find a standard deduction more valuable. Even if you exclude the tax benefit, the real cost of owning can still be less than renting.

-

Equity for you or equity for your landlord? With more or less equal payments, owning will always have an advantage in that you’re paying down principal and earning equity in your own home rather than the landlord's.

Thinking about making the move from renting to owning?

We can help you explore your options and find a path that works for your budget and goals. Call us at 888-616-9885 to get started or click 'get pre-approved' below to start your online pre-approval application.

.png)

----------------------------------------------------------------------

Factors used: $300,000 purchase price, 20% down, $240,000 fixed loan at 6.5%/6.822% APR. Principal and Interest payment = $1,517, taxes = $188/Mo., insurance = $50/Mo., and maintenance = $250/Mo. (1.00% of value). Tax deductibility at 20%. Tax savings, principal paid, and appreciation averaged over the first 12 months. Always consult with your tax advisor for advice specific to your situation. This is not an offer to lend. Rates, prices, taxes, insurance, etc., are all subject to regional and market differences and can change at any time. APR calculation is based on closing costs of 3% of the loan amount. Actual fees can be more or less.

*Federal Reserve, “Report on the Economic Well-Being of U.S. Households in 2024,” May 2025.